Key Takeaways

What You’ll Learn

- N26 operates as a digital neobank offering mobile-first banking and financial services.

- The company earns revenue through premium subscriptions, interchange fees, lending, and financial products.

- N26 combines banking, savings, investing, and payments into one digital ecosystem.

- Subscription-based banking plans help generate recurring revenue for the platform.

- Its mobile-first experience and simplified banking model helped N26 scale across Europe.

Stats That Matter

- N26 serves more than 8 million customers across multiple European markets.

- The company projected around €440 million in revenue for FY2024.

- N26 reached its first quarterly profit during 2024 as customer growth accelerated.

- Interest income and subscription services are becoming major revenue drivers for neobanks.

- Digital banking adoption continues increasing as users prefer mobile-first financial experiences.

Real Insights

- Neobanks grow faster when they simplify banking experiences for digital-first users.

- Premium subscription plans help fintech companies create predictable recurring revenue.

- Integrated investing, savings, and budgeting tools improve customer retention.

- Regulatory compliance and trust are critical for scaling digital banking platforms.

- Long-term fintech success depends on balancing customer growth, profitability, and operational efficiency.

Berlin-based neobank N26 is estimated to generate around €520 million in revenue in 2026, continuing strong growth after years of rapid user expansion and increasing monetization across its platform.

For founders and fintech builders, N26 provides a clear blueprint for building mobile-first financial platforms without physical branches. Understanding how N26 monetizes payments, subscriptions, and financial services reveals valuable insights for startups designing scalable fintech products.

N26 Revenue Overview – The Big Picture

N26 operates as a digital-only bank serving millions of users across Europe through a mobile banking app.

Financial Snapshot (2025–2026)

| Metric | Value |

|---|---|

| Estimated Revenue (2025) | ~€520 Million |

| Estimated Revenue (2026) | ~€620 Million |

| Estimated YoY Growth | ~18–20% |

| Valuation | ~$6 Billion |

| Active Customers | ~5.3 Million (est. 2025) |

| Countries Served | 24 |

N26’s growth is driven by strong adoption across Europe and rising financial activity on the platform, including payments, savings, and investment products.

Estimated Revenue Distribution by Region (2026)

| Region | Revenue Share |

|---|---|

| Germany | 32% |

| Western Europe | 43% |

| Southern Europe | 15% |

| Other EU Markets | 10% |

Benchmark Comparison

| Company | Estimated Revenue |

|---|---|

| Revolut | ~$2.5B |

| Monzo | ~$1B |

| N26 | ~€520M |

| bunq | ~$300M |

Despite being smaller than some competitors, N26 maintains strong growth due to high user engagement and low operating costs.

Read More: Business Model of N26: Complete Strategy Breakdown 2026

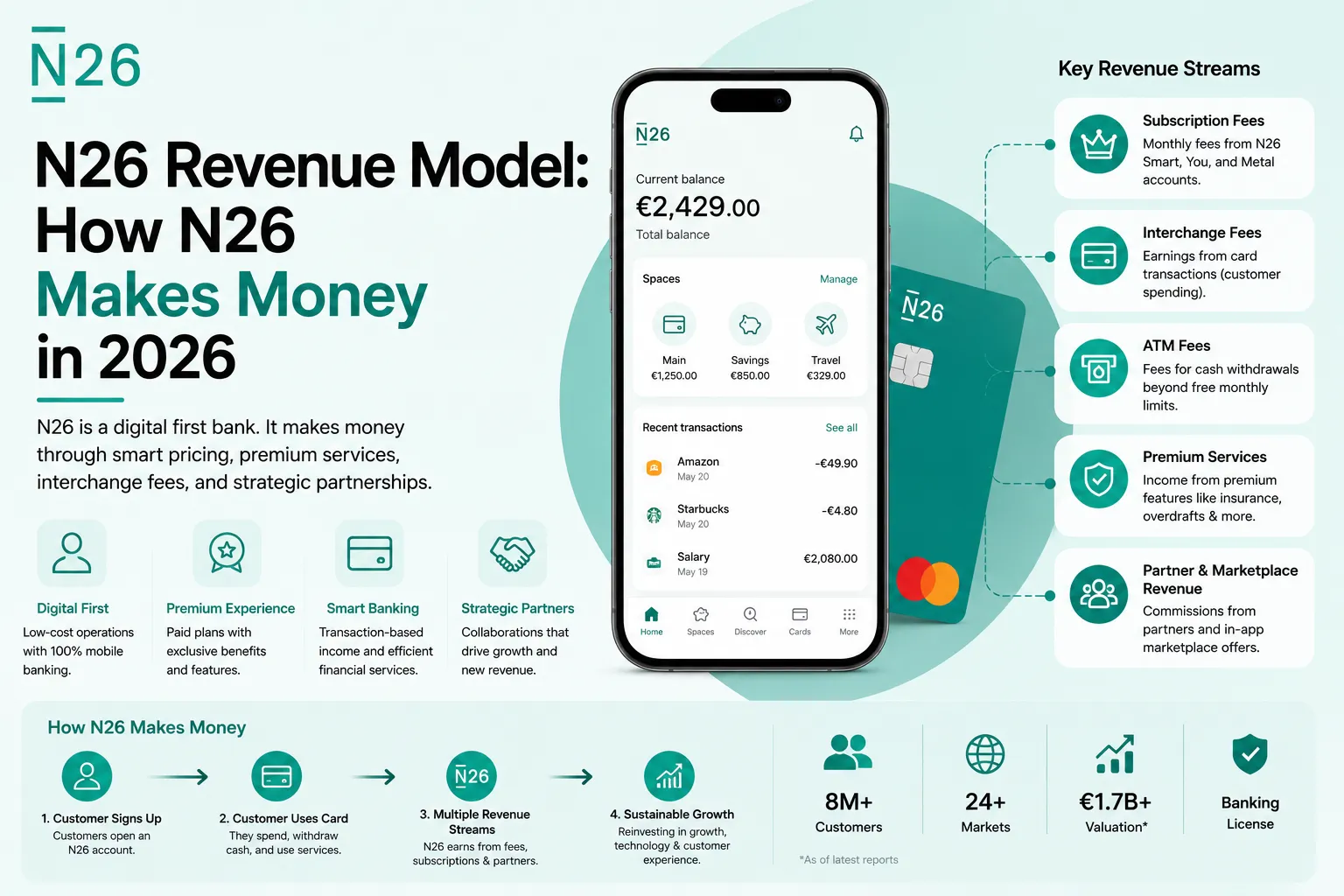

Primary Revenue Streams Deep Dive

N26 earns revenue through several monetization layers built around its digital banking platform.

Revenue Stream #1: Premium Subscription Plans

N26 offers paid subscription tiers with additional financial and lifestyle benefits.

Premium Plans (2026 Pricing)

| Plan | Monthly Price |

|---|---|

| Standard | Free |

| Smart | €4.90 |

| You | €9.90 |

| Metal | €16.90 |

Premium plans include:

• Travel insurance

• Higher withdrawal limits

• Premium debit cards

• Advanced analytics

• Savings features

Estimated revenue contribution: 35–40%

Subscription banking provides predictable recurring revenue, which stabilizes N26’s business model.

Revenue Stream #2: Interchange Fees

Whenever customers pay with their N26 card, the company earns a small fee from merchants.

Typical interchange fees in Europe:

0.2% – 0.3% per transaction

With billions in yearly payment volume across the platform, these micro-fees add up to significant revenue.

Estimated contribution: 30%

Revenue Stream #3: Interest Income

As a licensed bank, N26 earns money from:

• Customer deposits

• Treasury management

• Lending products

Interest income has become a major driver as interest rates increased across Europe.

Estimated contribution: 20–25%

Revenue Stream #4: Partner Financial Products

N26 generates additional revenue through partnerships such as:

• Insurance products

• Crypto trading

• Stock and ETF investing

• Buy-now-pay-later services

N26 receives referral commissions or revenue shares from these financial partners.

Estimated contribution: 8–10%

Revenue Stream #5: ATM and Foreign Exchange Fees

While N26 offers free withdrawals in certain plans, additional ATM withdrawals or foreign transactions may incur fees.

Estimated contribution: 5%

Revenue Streams Breakdown (Latest Available Data)

| Revenue Stream | Description | Estimated Revenue Share | Pricing Model |

|---|---|---|---|

| Premium Subscriptions | Paid banking tiers | 35–40% | Monthly subscription |

| Interchange Fees | Merchant fees from card payments | ~30% | % per transaction |

| Interest Income | Deposits and lending | 20–25% | Interest margin |

| Partner Products | Insurance, crypto, investments | 8–10% | Revenue share |

| ATM / FX Fees | Withdrawals and currency exchange | ~5% | Transaction fees |

The Fee Structure Explained

N26 monetizes both users and financial partners through layered fee structures.

Platform Fee Structure (Latest Available Data)

| User Type | Fee Type | Typical Fee Range | Notes |

|---|---|---|---|

| Free Users | ATM withdrawals | €2 – €5 after limits | Limited free withdrawals |

| Premium Users | Monthly subscription | €4.90 – €16.90 | Core monetization |

| Merchants | Interchange fee | 0.2–0.3% | Paid by merchant banks |

| Investors | Trading commissions | Small transaction fees | Via investment partners |

| International Users | FX fees | ~1–2% | Currency conversion |

Hidden revenue layers include:

• Investment platform commissions

• Crypto trading spreads

• Partner marketplace revenue

How N26 Maximizes Revenue Per User

N26 focuses heavily on ARPU (Average Revenue Per User) growth.

Key Monetization Strategies

Customer Segmentation

Users are segmented into:

• Free users

• Premium subscribers

• High-value banking users

Premium users generate significantly higher revenue through subscriptions and financial activity.

Upselling Mechanics

N26 constantly encourages upgrades from free accounts to premium plans by offering:

• Travel benefits

• Higher savings interest

• Insurance packages

Cross-Selling

Users can access:

• Stock trading

• Crypto trading

• Savings products

• Loans

These financial tools increase customer lifetime value.

Retention Monetization

N26 integrates multiple financial services into a single app, increasing platform stickiness and long-term engagement.

Cost Structure & Profit Margins

Digital banks operate with lower infrastructure costs compared to traditional banks.

Major Cost Categories

| Cost Category | Description |

|---|---|

| Technology Infrastructure | Cloud banking systems |

| Compliance | Anti-money laundering & regulation |

| Marketing | User acquisition |

| Customer Support | Global service operations |

| Product Development | Fintech innovation |

Because N26 has no physical branches, operational costs are significantly lower than traditional banks.

Unit Economics

Key metrics influencing profitability:

• Customer acquisition cost (CAC)

• Average revenue per user (ARPU)

• Transaction volume per customer

Strong word-of-mouth growth helps keep CAC relatively low.

Future Revenue Opportunities (2026–2028 Outlook)

Several growth opportunities exist for N26.

Potential Expansion Areas

1. SME Banking

Business accounts could unlock a large new revenue stream.

2. Embedded Finance

N26 may integrate financial services into third-party platforms.

3. Lending Expansion

Consumer loans and credit products could significantly increase revenue.

4. AI-Driven Financial Advice

AI financial assistants could drive new subscription tiers.

Market Risks

• Regulatory scrutiny

• Competition from Revolut and traditional banks

• Rising compliance costs

Lessons for Entrepreneurs

Founders can learn several powerful lessons from N26.

What Works Well

• Mobile-first product design

• Subscription monetization

• Marketplace-style financial services

What Startups Can Replicate

• Premium subscription tiers

• Interchange-based monetization

• Financial product marketplaces

Market Gaps

Opportunities still exist in:

• SME fintech tools

• AI financial planning apps

• Cross-border banking solutions

Miracuves N26-Like Digital Banking Platform Solution Cost and Tech Stack

Miracuves Pricing for an N26-Like Digital Banking Platform developed using Node.js / React.js Architecture is available on request. Contact Miracuves for custom pricing based on platform features, scalability requirements, banking integrations, compliance scope, and deployment infrastructure. Estimated delivery timeline: 30 to 90 Days.

Build a powerful digital banking and fintech platform designed for startups, neobanks, fintech companies, payment providers, and enterprise financial operations.

Core Workflows: Digital account management, virtual and physical card operations, money transfers, transaction tracking, budgeting tools, savings management, and mobile-first banking workflows.

Built-in Finance: Payment processing, real-time transaction monitoring, IBAN and banking integrations, KYC and AML workflows, expense analytics, subscription tracking, and financial reporting systems.

Management Hub: Admin dashboards, customer management systems, compliance controls, fraud monitoring, analytics reporting, audit logs, card management systems, and centralized banking operations management.

Enterprise-Ready: Fully customizable architecture prepared for secure scaling, multi-region banking operations, compliance-ready infrastructure, high-volume financial transactions, and long-term fintech platform growth.

Why does an N26-Like Platform require Node.js / React.js architecture?

Digital banking platforms process real-time financial transactions, payment operations, compliance workflows, and secure customer account management systems. These platforms require scalable infrastructure, low-latency financial processing, and highly responsive interfaces across web and mobile ecosystems.

We recommend a modern JavaScript-based architecture for this type of platform because:

Built for Real-Time Operations: Node.js enables scalable backend operations for instant payments, transaction processing, account synchronization, fraud monitoring, and concurrent banking activities.

Advanced Dashboard Experience: React.js supports highly interactive interfaces for banking dashboards, transaction analytics, card management, budgeting tools, and seamless customer experiences.

Enterprise Scalability: This architecture is well-suited for handling high-volume financial operations, multi-user banking ecosystems, compliance workflows, and rapidly growing fintech platforms.

Flexible Integration Layer: Easily integrates with banking APIs, payment gateways, KYC and AML providers, card issuing systems, fraud detection tools, analytics platforms, and financial infrastructure services.

You get a scalable, enterprise-grade digital banking platform designed for long-term operational growth.

Note: Final pricing depends on banking modules, compliance requirements, third-party integrations, deployment infrastructure, security systems, and custom workflow development.

Conclusion

N26 proves that banking no longer needs to rely on physical branches or legacy infrastructure to scale. By combining mobile-first design, subscription revenue, and a financial marketplace ecosystem, the company has created a flexible digital banking platform that can continuously expand into new financial services.

For founders and fintech builders, the biggest lesson is clear: the future of banking belongs to platforms that prioritize technology, user experience, and ecosystem-driven monetization. Startups that can integrate multiple financial services into a seamless digital experience have the potential to build the next generation of global fintech platforms.

FAQs

1. How much does N26 make per transaction?

Typically 0.2–0.3% interchange fee on card transactions.

2. What is the most profitable revenue stream for N26?

Premium subscriptions and interest income are currently the largest profit drivers.

3. How does N26 pricing compare to competitors?

N26 offers simpler and lower-cost banking plans compared to many competitors. While platforms like Revolut and Wise provide more advanced international transfer and multi-currency features, N26 focuses on affordable digital banking with straightforward pricing, low fees, and easy everyday banking services.

4. What percentage does N26 take from providers?

Partner financial products usually involve revenue-sharing commissions.

5. How has N26’s revenue model evolved?

Initially focused on interchange fees, the model has expanded to include subscriptions, lending, and investment services.

6. Can small startups use a similar model?

Yes. Many fintech startups adopt subscription + interchange hybrid models.

7. What scale is needed for profitability?

Typically millions of active users due to thin payment margins.

8. How can founders implement a similar model?

By combining:

• Digital banking infrastructure

• Payment monetization

• Financial service marketplaces

9. What alternatives exist to this revenue model today?

Alternative fintech models include:

• Credit-first fintech platforms

• Payment-processing companies

• Banking-as-a-service platforms