The business model of SoFi (Social Finance) represents one of the most compelling fintech transformations of the last decade. What began as a student loan refinancing startup has evolved into a full-scale digital financial ecosystem offering lending, banking, investing, credit cards, and enterprise fintech infrastructure.

At the core of SoFi’s success is a hybrid platform strategy that blends consumer financial services with high-margin B2B technology solutions. By combining traditional revenue streams like lending with recurring income from banking services and fintech APIs, SoFi reduced its dependence on any single product line.

For entrepreneurs and product leaders, studying the SoFi business model offers valuable lessons in platform design, monetization, and long-term scalability. It demonstrates how trust, technology, and strategic expansion can transform a niche fintech idea into a sustainable, billion-dollar digital business.

How the SoFi Business Model Works

SoFi business model is best understood as a layered fintech ecosystem, not a single financial product. What began as a lending company has evolved into a hybrid platform that blends consumer finance, subscriptions, and B2B financial infrastructure under one brand.

At its core, SoFi is designed to capture a customer early, expand across life stages, and monetize across multiple verticals over time—a classic lifetime value (LTV) maximization play.

Business Model Type

SoFi operates a Hybrid Business Model, combining:

- Direct-to-Consumer Fintech Platform (B2C)

- Subscription-Based Membership Model

- Technology-as-a-Service Platform (B2B via Galileo & Technisys)

This hybridization is what allows SoFi to remain resilient even when one segment (like lending) faces macroeconomic pressure.

Value Proposition by User Segment

SoFi doesn’t sell “products”—it sells financial simplicity and progression.

1. Consumers (Primary Segment)

- One app for borrowing, saving, spending, investing, and financial planning

- Lower fees, competitive rates, and modern UX

- Incentives for bundling products (rate discounts, rewards, bonuses)

2. Financial Institutions & Fintechs (B2B Segment)

- Access to SoFi’s backend infrastructure via Galileo (payments, APIs) and Technisys (core banking)

- Faster time-to-market without building banking tech from scratch

3. Partners & Merchants

- Distribution access to SoFi’s high-income, digitally native member base

- Embedded finance opportunities inside the ecosystem

Key Stakeholders & Their Roles

- Members: Drive transaction volume, deposits, and cross-product usage

- SoFi Bank: Enables margin expansion via deposit-based funding

- Technology Clients (Galileo/Technisys): Provide stable, recurring B2B revenue

- Regulators: Shape compliance-driven trust and long-term defensibility

- Investors: Support capital-intensive lending and platform scaling

Maintaining balance between these stakeholders is critical—SoFi’s banking charter plays a central role here.

How the Model Evolved Over Time

SoFi’s evolution followed a deliberate path:

- Single-product focus: Student loan refinancing

- Product expansion: Personal loans, mortgages, investing

- Platform unification: One app, one member identity

- Vertical integration: Banking charter + deposits

- Ecosystem expansion: B2B fintech infrastructure (Galileo, Technisys)

Each phase reduced dependency on any single revenue stream.

Why This Model Works in 2026

SoFi’s structure aligns perfectly with 2026 market realities:

- Consumers prefer all-in-one financial super apps

- Rising CAC makes cross-selling cheaper than new acquisition

- Deposits are more valuable amid volatile interest rates

- Fintech infrastructure demand is surging globally

- Trust, compliance, and scale now matter more than “growth at all costs”

This is exactly the kind of future-proof platform architecture Miracuves helps founders design—models that can add verticals without breaking the core experience.

Read more : What is SoFi App and How Does It Work?

Target Market & Customer Segmentation Strategy

SoFi’s growth isn’t driven by mass-market appeal—it’s driven by precision targeting. From day one, SoFi focused on a financially upward, digitally savvy audience and then expanded horizontally across their financial lives.

Instead of chasing everyone, SoFi optimized for high lifetime value members who would adopt multiple products over time.

Primary Customer Segments

1. Emerging Professionals (Core Segment)

- Age: ~22–40

- Profile: College-educated, early to mid-career, rising income

- Needs: Student loan refinancing, personal loans, banking, investing

- Behavior: Mobile-first, brand-loyal, financially proactive

This segment delivers the highest cross-sell and retention rates, making it the backbone of SoFi’s unit economics.

2. Affluent & Mass-Affluent Consumers

- Higher deposits and investment balances

- Use SoFi for high-yield checking/savings, credit cards, and wealth tools

- Lower churn due to ecosystem stickiness

3. Fintech & Financial Institutions (B2B)

- Startups, neobanks, traditional banks modernizing their stack

- Use Galileo APIs and Technisys core banking

- Long-term contracts = predictable recurring revenue

Secondary Segments

- Gig economy professionals seeking flexible finance

- First-time investors entering crypto, ETFs, and fractional shares

- Small-scale entrepreneurs using SoFi for personal–business financial overlap

Customer Journey: Discovery → Conversion → Retention

1. Discovery

- Content marketing (financial education, SEO)

- Employer partnerships and alumni networks

- App store visibility and referral incentives

2. Conversion

- Frictionless onboarding

- Aggressive welcome bonuses (direct deposit, account funding)

- Rate discounts for bundled products

3. Retention & Expansion

- Product bundling rewards

- Unified financial dashboard

- Gamified savings and investing nudges

- Personalized recommendations powered by behavioral data

Retention is where SoFi wins: each additional product dramatically increases member LTV while reducing churn.

Acquisition Channels & LTV Optimization

- Paid digital ads → flagship product entry (loans or banking)

- Referral loops with cash rewards

- Employer and ecosystem partnerships

- In-app cross-promotion replaces external CAC over time

SoFi’s real acquisition advantage?

Market Positioning & Competitive Edge

SoFi positions itself as:

- “The financial partner for ambitious professionals”

- More holistic than single-product fintechs

- More digital and user-centric than traditional banks

Differentiation Strategies

- One-member, multi-product identity

- Strong brand voice: empowering, modern, aspirational

- Banking charter + fintech agility

- Data-driven personalization across verticals

This positioning allows SoFi to compete with banks, brokers, and fintech startups simultaneously—without being boxed into one category.

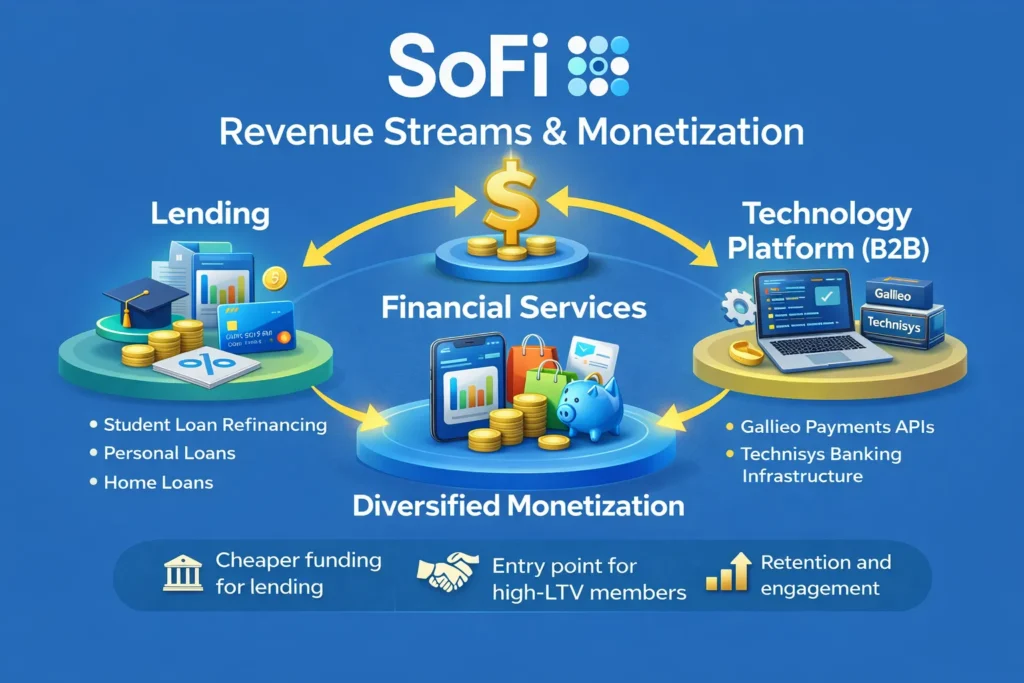

Revenue Streams & Monetization Design

SoFi’s monetization strategy is built around diversification + compounding value per member. Instead of relying on a single revenue engine, SoFi designed a system where multiple revenue streams reinforce each other—making the business more resilient across economic cycles.

At a high level, revenue flows from three interconnected pillars:

- Lending

- Financial Services

- Technology Platform (B2B)

Primary Revenue Stream: Lending Products

Lending remains SoFi’s largest revenue contributor, though its relative share has declined as the platform diversified.

Key Lending Verticals

- Student loan refinancing

- Personal loans

- Home loans (selective focus)

How it makes money

- Net interest income (spread between borrowing cost and lending rate)

- Origination fees

- Loan sales to institutional investors

Why it still matters in 2026

- Personal loans continue to grow despite rate cycles

- SoFi’s deposit base lowers cost of capital

- High-credit-quality members reduce default risk

Growth trajectory: Lending is now optimized for profitability and risk control, not raw volume.

Secondary Revenue Stream 1: Financial Services (Banking, Investing, Cards)

This segment is all about recurring engagement and margin expansion.

Components

- Checking & savings accounts

- Credit cards

- Investment products (ETFs, stocks, crypto)

- Subscription-style financial planning tools

Monetization Mechanics

- Interchange fees from card usage

- Interest income on deposits

- Margin on investment services

- Subscription-style premium features (SoFi Plus–style benefits)

While individual transactions may be small, this segment:

- Improves retention

- Increases data depth

- Fuels cross-selling into higher-margin products

Secondary Revenue Stream 2: Technology Platform (Galileo + Technisys)

This is SoFi’s most strategically important long-term revenue engine.

What it includes

- Galileo: Payments processing, account APIs, card issuing

- Technisys: Core banking infrastructure for digital banks

Revenue Model

- Usage-based pricing (API calls, transactions)

- Long-term SaaS-style contracts

- Enterprise onboarding and customization fees

Why founders should pay attention

- High gross margins

- Predictable, recurring revenue

- Decoupled from consumer credit cycles

This B2B layer transforms SoFi from a fintech app into a fintech infrastructure company.

How the Monetization System Fits Together

SoFi’s brilliance lies in how these streams interlock:

- Banking products → cheaper funding for lending

- Lending → entry point for high-LTV members

- Financial services → retention and engagement

- Technology platform → margin stability and valuation multiple expansion

Cross-Selling & Upselling Tactics

- Rate discounts for bundled products

- Rewards for direct deposit adoption

- In-app nudges based on lifecycle triggers

Behavioral pricing psychology (simple tiers, visible benefits)

Operational Model & Key Activities

SoFi’s real competitive strength isn’t just what it offers—it’s how efficiently it operates a highly regulated, multi-product fintech platform at scale. Its operating model is designed to balance speed, compliance, and cost discipline, which is notoriously difficult in financial services.

At a glance, SoFi runs like a technology company with a bank license, not a traditional bank with a digital app.

Core Operational Pillars

1. Platform & Product Management

- Single unified app across banking, lending, and investing

- Modular product architecture allows rapid feature rollout

- Continuous UX optimization driven by member behavior data

2. Technology Infrastructure

- Cloud-native architecture

- Shared backend services across all products

- Internal risk, fraud, and compliance engines

- API-first mindset (same tech powering B2C and B2B)

This shared infrastructure is what enables economies of scale as new products are added.

Risk, Compliance & Quality Control

- Centralized credit underwriting models

- Real-time fraud detection and AML systems

- Regulatory reporting embedded into workflows

- Banking charter enables direct oversight instead of dependency on partner banks

While compliance is often seen as a cost, SoFi treats it as a trust and moat-building function.

Customer Support & Experience Operations

- In-app support and AI-assisted help centers

- Tiered human support for high-value members

- Feedback loops tied directly to product teams

This keeps service costs lower while maintaining high satisfaction among premium users.

Marketing & Growth Operations

- Performance marketing tightly tracked to LTV

- Heavy reliance on cross-sell vs constant new-user acquisition

- Brand partnerships and major sponsorships to reinforce trust (e.g., sports, finance education)

Resource Allocation Strategy (High-Level)

SoFi’s spending is deliberately skewed toward long-term platform leverage:

- Technology & Product: ~40%

- Marketing & Growth: ~20–25%

- Risk, Compliance & Operations: ~15–20%

- R&D & Innovation: ~10–15%

- Geographic & Product Expansion: Opportunistic, data-driven

This allocation reflects a belief that software efficiency + data intelligence ultimately outperforms branch-heavy banking models.

Why This Operating Model Scales

- One tech stack supports multiple revenue lines

- Marginal cost per additional product is low

- Compliance investment compounds trust

- B2B infrastructure reuses internal systems for external revenue

This is exactly the operational blueprint Miracuves applies when helping founders move from MVP → regulated platform → scalable ecosystem.

Strategic Partnerships & Ecosystem Development

SoFi’s leadership understands a critical platform truth:

you don’t scale ecosystems alone—you orchestrate them.

Rather than building everything in-house, SoFi uses partnerships to accelerate reach, deepen capabilities, and reinforce network effects, all while keeping control of the core user experience.

SoFi’s Partnership Philosophy

SoFi partners where:

- Speed to market matters more than ownership

- External scale can be leveraged faster than internal build

- Partnerships enhance trust, compliance, or distribution

At the same time, SoFi keeps customer data, UX, and platform intelligence in-house, ensuring it never becomes dependent on any single partner.

Key Partnership Categories

1. Technology & API Partners

- Cloud infrastructure providers

- Data and analytics vendors

- Security and identity verification platforms

- Open banking and payment rails integrations

These partnerships allow SoFi to ship features quickly while maintaining enterprise-grade reliability.

2. Payment, Banking & Financial Alliances

- Card networks (Visa, Mastercard)

- Payment processors and clearing networks

- Liquidity and capital market partners

These alliances support transaction scale while SoFi’s banking charter reduces reliance on intermediaries over time.

3. B2B Ecosystem Clients (Reverse Partnerships)

- Fintech startups using Galileo APIs

- Digital banks running on Technisys core banking

- Enterprises embedding finance into non-financial products

Here, customers become ecosystem partners, strengthening SoFi’s platform gravity.

4. Marketing & Distribution Partnerships

- Employer benefit programs

- Education and alumni networks

- High-visibility brand partnerships (sports, finance education)

These lower CAC while boosting brand credibility—crucial in financial services.

5. Regulatory & Expansion Alliances

- Federal and state regulatory bodies

- International compliance partners

- Local banking collaborators for market entry

Rather than fighting regulation, SoFi integrates regulators into its scaling strategy.

Ecosystem Strategy: The Real Moat

SoFi’s ecosystem creates multi-layered defensibility:

- Network effects: More members → more data → better products

- Partner lock-in: B2B clients build on SoFi infrastructure

- Monetization at multiple layers: Consumer, enterprise, platform

Switching costs: Both users and partners face friction leaving the ecosystem

Read more : Best SoFi Clone Scripts 2026: Build a Next-Gen Digital Banking & Lending Platform

Growth Strategy & Scaling Mechanisms

SoFi’s growth playbook is a disciplined blend of virality, financial incentives, product expansion, and geographic leverage. Unlike many fintechs that chased user numbers at any cost, SoFi optimized for profitable, repeatable growth loops.

Its strategy answers one key question:

How do we grow faster while becoming more efficient each year?

SoFi’s Core Growth Engines

1. Organic Virality & Referral Loops

- Cash-based referral rewards

- Product-linked incentives (fund an account → earn rewards)

- Social proof from community and employer programs

Each successful referral lowers CAC while reinforcing trust.

2. Paid Acquisition with LTV Discipline

- Performance marketing tied directly to product adoption, not just sign-ups

- Entry-point products (banking or loans) act as conversion funnels

- Rapid pruning of unprofitable channels

SoFi spends where multi-product adoption probability is highest.

3. Product-Led Expansion

- New financial products introduced to existing members first

- Minimal external marketing for add-ons

- Personalized in-app offers triggered by life events

This turns the app into a self-expanding revenue engine.

4. Geographic & Market Expansion

- Focus on regulatory-ready markets

- Leverages existing tech stack for new regions

- Selective international exposure via B2B tech clients

Instead of rushing global consumer expansion, SoFi lets its infrastructure scale globally first.

Scaling Challenges & How SoFi Solved Them

Challenge 1: Interest Rate Volatility

- Solution: Banking charter + deposit funding

- Outcome: Lower cost of capital and higher margins

Challenge 2: Operational Complexity

- Solution: Unified tech stack and shared services

- Outcome: Reduced marginal costs per product

Challenge 3: Regulatory Pressure

- Solution: Proactive compliance investment

- Outcome: Increased trust and market credibility

Challenge 4: Market Cycles in Lending

- Solution: B2B tech revenue diversification

- Outcome: Stability during downturns

Why This Growth Model Works

- Growth is tied to usage, not hype

- New revenue streams don’t require new users

- Infrastructure investments compound over time

- Risk is spread across multiple verticals

This mirrors how Miracuves helps founders design scaling frameworks that don’t collapse under success—growth systems that mature rather than burn out.

Competitive Strategy & Market Defense

SoFi operates in one of the most competitive environments in business—financial services, where incumbents are massive, startups are aggressive, and regulation raises the cost of failure.

SoFi’s defense strategy is not about blocking competitors outright—it’s about making competition increasingly inefficient.

Core Competitive Advantages

1. Network Effects & Switching Barriers

- Multi-product usage increases lock-in

- Unified financial data creates personalization advantages

- Members using 3+ products show dramatically lower churn

The more value SoFi delivers, the harder it is to replace.

2. Brand Equity & Trust

- Positioned as a financial ally, not a bank

- Transparent pricing and modern UX

- Regulatory credibility through banking charter

In finance, trust compounds faster than features.

3. Technology & Platform Innovation

- Shared infrastructure across products

- Rapid feature experimentation

- Continuous backend optimization

This allows SoFi to move faster than traditional banks—and cheaper than single-product fintechs.

4. Data-Driven Personalization

- Behavioral insights across spending, saving, borrowing, investing

- Predictive offers tied to life-stage transitions

- Smarter underwriting and risk scoring

Data depth becomes a self-reinforcing moat.

Market Defense Tactics

Handling New Entrants

- Bundling products to undercut single-feature competitors

- Offering incentives incumbents can’t match without margin pain

Pricing & Feature Wars

- Uses cross-subsidization across verticals

- Keeps headline pricing attractive while monetizing elsewhere

Strategic Timing

- Rolls out features when competitors are capital-constrained

- Invests in infrastructure during downturns

Acquisitions & Partnerships

- Acquires capabilities that accelerate roadmap (e.g., tech platforms)

- Partners where acquisition isn’t capital-efficient

Why This Defense Holds in 2026

- Regulation raises barriers for newcomers

- Consumers prefer fewer financial apps

- Capital markets reward diversified revenue

- Infrastructure-led fintechs scale better than niche apps

For founders, the lesson is clear: defensibility is designed early, not added later—a principle Miracuves embeds from day one in platform architecture.

Lessons for Entrepreneurs & Implementation

If SoFi’s journey teaches one overarching lesson, it’s this:

the biggest fintech winners aren’t single-product apps—they’re platforms designed to grow with their users.

Below is a founder-focused breakdown of what to copy, what to adapt, and what to avoid.

Key Factors Behind SoFi’s Success

- Lifecycle-first thinking: Capture users early and grow with them

- Multi-revenue design: Lending, services, and infrastructure reinforce each other

- Tech-led operations: Built like a software company, regulated like a bank

- Relentless cross-selling: Lower CAC over time

- Trust as strategy: Compliance and transparency as growth levers

Replicable Principles for Startups

You don’t need SoFi’s scale to apply its principles:

- Start with one painful financial problem

- Design the architecture to support future products

- Centralize user identity and data early

- Optimize for LTV, not vanity growth

- Treat regulation as a moat, not a blocker

These principles apply beyond fintech—to marketplaces, super apps, and SaaS platforms.

Common Mistakes to Avoid

- Launching too many products too early

- Ignoring compliance until it’s “required”

- Over-reliance on paid acquisition

- Fragmented UX across features

- Monetizing before trust is earned

Many startups fail not because of lack of demand—but because their model can’t scale cleanly.

Adapting the Model for Local or Niche Markets

SoFi’s model can be localized by:

- Focusing on one core product first (e.g., lending or payments)

- Partnering instead of acquiring licenses early

- Building vertical-specific fintechs (creators, SMEs, gig workers)

- Using B2B infrastructure to fund consumer growth

Implementation & Investment Priorities

Phase 1 :

- Core product + compliance foundation

- MVP with scalable backend

Phase 2 :

- Add 1–2 complementary services

- Introduce cross-selling and referrals

Phase 3 :

- Platform expansion

- B2B or infrastructure monetization

- Regional scaling

This staged approach mirrors how Miracuves helps founders move from idea → product → platform without overextending capital.

Ready to implement SoFi’s proven business model for your market?

Miracuves builds scalable platforms with tested business models and growth mechanisms. We’ve helped 200+ entrepreneurs launch profitable apps.

Get your free business model consultation today.

Conclusion

SoFi’s journey proves that innovation alone doesn’t build enduring companies—execution at scale does. By combining financial products, infrastructure, and data into a single cohesive platform, SoFi moved beyond being “another fintech app” and became a financial operating system for modern consumers.

In a world where customer trust is fragile, acquisition costs are rising, and regulation is unavoidable, SoFi shows what happens when strategy, technology, and discipline move in sync. The real win wasn’t faster growth—it was smarter growth.

As we look toward 2026 and beyond, platform economies will continue to favor companies that: Build lasting growth by owning the customer relationship, monetizing across multiple layers, and designing ecosystems—not just individual features.

FAQs

What type of business model does SoFi use?

SoFi uses a hybrid fintech platform model combining B2C financial services, subscriptions, and B2B financial infrastructure.

How does SoFi’s business model create value?

By offering multiple financial products in one ecosystem, SoFi increases convenience, reduces costs, and grows lifetime value per member.

What are SoFi’s key success factors?

Cross-selling, technology-driven operations, diversified revenue streams, strong compliance, and a clear target audience.

How scalable is the SoFi business model?

Highly scalable. Its shared tech stack supports new products and markets with low marginal cost.

What are the biggest challenges in SoFi’s model?

Regulatory complexity, credit risk management, and balancing growth with profitability.

How can entrepreneurs adapt SoFi’s model to their region?

Start with one core product, partner for compliance, and expand vertically once trust and data scale.

What are alternatives to SoFi’s business model?

Single-product fintechs, niche vertical banks, or SaaS-only financial infrastructure platforms.

How has SoFi’s business model evolved over time?

It evolved from student loan refinancing into a multi-product fintech ecosystem with a strong B2B infrastructure layer.

Related Article :

- What is a Revolut App and How Does It Work?

- What is Monzo App and How Does It Work?

- Best Stripe Clone Scripts 2025: Build a Scalable Global Payment Infrastructure for Your Startup

- Best N26 Clone Scripts 2026 for Digital Banking Startups

- Best Monzo Clone Scripts 2026: Build a Digital Banking App That Scales Globally