Key Takeaways

What You’ll Learn

- Affirm operates on a Buy Now, Pay Later (BNPL) fintech business model.

- The company earns revenue through merchant fees, interest income, interchange fees, and loan servicing.

- Affirm partners with ecommerce businesses to offer flexible installment payment options.

- AI-driven underwriting and risk assessment help improve approval speed and credit management.

- Transparent payment structures and no late fees helped Affirm differentiate itself in the BNPL market.

Stats That Matter

- Affirm reported more than 26 million active users and over $37 billion in annual payment volume.

- The company generates revenue from merchant discount fees and consumer loan interest.

- Affirm’s revenue crossed $4 billion annually with strong BNPL transaction growth.

- BNPL adoption continues growing globally as ecommerce and flexible financing demand increase.

- Affirm’s merchant partnerships and consumer transaction volume continue expanding across ecommerce sectors.

Real Insights

- BNPL platforms grow faster when they balance merchant benefits with consumer trust.

- Transparent pricing and flexible installment plans improve customer adoption.

- AI-powered credit assessment helps fintech companies scale lending operations more efficiently.

- Partnerships with major ecommerce platforms create significant transaction growth opportunities.

- Long-term BNPL success depends on sustainable underwriting, compliance, and customer retention.

In less than a decade, Affirm transformed from a fintech startup into a publicly traded company worth tens of billions, powering millions of consumer transactions annually across e-commerce platforms.

Founded by Max Levchin (PayPal co-founder), Affirm reimagined credit by replacing hidden fees and revolving debt with transparent installment financing. Instead of traditional credit cards with compounding interest, Affirm allows consumers to split purchases into predictable payments at checkout. Today in 2026, Affirm operates at the center of the Buy Now, Pay Later (BNPL) revolution, partnering with major brands such as: Amazon ,Shopify merchants ,Walmart ,Peloton

This model has become a blueprint for modern fintech platforms, especially those blending embedded finance, marketplace dynamics, and data-driven credit underwriting. For entrepreneurs exploring fintech, lending platforms, or embedded payment ecosystems, understanding the business model of Affirm reveals how financial infrastructure companies scale globally. And for companies like Miracuves, which specialize in building scalable digital platforms and fintech ecosystems, Affirm provides a powerful case study in designing platform-first financial services.

How the Affirm Business Model Works

At its core, Affirm operates as a fintech-enabled credit marketplace that connects consumers, merchants, and capital providers through a transparent installment payment system.

Instead of traditional credit cards that revolve debt and charge hidden fees, Affirm integrates directly into the checkout process of online and offline retailers, allowing customers to split purchases into fixed installment payments. The platform earns revenue primarily from merchant fees and consumer interest, while its underwriting engine evaluates credit risk using real-time financial data and machine learning models.

The brilliance of the Affirm model lies in how it aligns incentives:

- Consumers get flexible payments without hidden charges

- Merchants increase conversions and average order value

- Affirm monetizes financing and transaction infrastructure

In essence, Affirm is not just a lender — it is a payment infrastructure layer embedded into commerce platforms.

Type of Business Model

Affirm uses a Hybrid Fintech Platform Model combining several structures:

1. BNPL Lending Model

- Provides installment loans at checkout.

- Consumers pay over time with fixed terms.

2. Two-Sided Marketplace

- Connects merchants and consumers through the payment platform.

3. Embedded Finance Platform

- Integrates financing directly into merchant checkout systems via APIs.

4. Financial Infrastructure Model

- Partners with banks and institutional investors to fund loans.

This hybrid approach allows Affirm to scale like a software platform while monetizing like a financial institution

Evolution of the Model

Affirm’s business model has evolved significantly since launch.

Phase 1: Consumer Financing (2012–2017)

Affirm focused on simple installment loans for e-commerce purchases.

Phase 2: Merchant Platform Expansion (2018–2021)

The company integrated with major platforms like Shopify, allowing thousands of merchants to offer BNPL.

Phase 3: Financial Ecosystem (2022–2024)

Affirm expanded into:

- Debit cards

- Savings products

- Merchant tools

- Consumer shopping apps

Phase 4: Embedded Finance Infrastructure (2025–2026)

Today Affirm operates as a financial platform embedded inside digital commerce ecosystems, powering payments for large marketplaces and retail platforms.

Why the Model Works in 2026

Several macro trends are driving Affirm’s continued growth:

Shift Away From Credit Cards

Younger consumers prefer transparent financing instead of revolving debt.

E-commerce Growth

Online commerce continues to expand globally, increasing demand for embedded payment solutions.

Checkout Financing as Conversion Tool

Retailers increasingly view financing options as a sales optimization strategy rather than just a payment method.

Embedded Finance Boom

Platforms across industries now embed financial services directly into their ecosystems.

Read more : What is Affirm and How Does It Work?

Target Market & Customer Segmentation Strategy

To understand why Affirm scales so effectively, it’s critical to analyze who uses the platform and how those users interact with it.

Affirm’s growth strategy focuses on digitally native consumers and online-first merchants, particularly in high-ticket e-commerce categories where flexible financing significantly improves purchasing decisions.

The company uses data-driven segmentation and embedded checkout integrations to reach customers exactly when they are ready to buy.

Primary Customer Segments

Affirm’s ecosystem revolves around two main user groups.

1. Consumers (Borrowers)

The largest segment consists of consumers looking for transparent financing options at checkout.

Key demographics include:

- Gen Z and Millennials

- Online-first shoppers

- Consumers avoiding traditional credit cards

- Buyers making large discretionary purchases

Common purchase categories include:

- Electronics

- Fitness equipment

- Travel

- Furniture

- Fashion

- Education services

Many users adopt Affirm because they prefer predictable installment payments instead of revolving credit debt.

Behavior patterns show that these consumers:

- Shop primarily online

- Value financial transparency

- Prefer mobile-first payment experiences

- Respond well to flexible financing options

2. Merchants (Retail Partners)

Affirm’s second core segment is e-commerce merchants and retail brands.

Typical merchant partners include:

- Direct-to-consumer brands

- Online retailers

- Enterprise marketplaces

- Subscription-based services

- Travel and experience platforms

Merchants adopt Affirm primarily to:

- Increase checkout conversions

- Raise average order value (AOV)

- Reduce cart abandonment

- Offer financing without managing credit risk

In many cases, merchants see AOV increase by 40–85% when BNPL is offered.

Secondary Customer Segments

Affirm also serves additional stakeholders who support the financial ecosystem.

Institutional Capital Partners

Banks and asset managers fund many of the loans originated through Affirm’s platform.

Their motivations include:

- Access to consumer credit portfolios

- Data-driven risk underwriting

- Portfolio diversification

Platform Partners

Affirm integrates with major commerce platforms including:

- Shopify

- Amazon

- Walmart

- WooCommerce

- BigCommerce

These integrations allow Affirm to scale across millions of online stores simultaneously.

Customer Journey: From Discovery to Retention

Affirm’s growth engine is built around the checkout moment, when purchasing intent is highest.

Stage 1 – Discovery

Customers discover Affirm through:

- Checkout payment options

- Merchant promotions

- Mobile shopping apps

- Affirm’s consumer marketplace app

Stage 2 – Conversion

At checkout, users see a financing offer such as:

- “Pay $60/month for 6 months”

Affirm’s real-time underwriting engine approves loans within seconds.

This instant approval significantly increases purchase completion rates.

Stage 3 – Engagement

After the purchase:

- Customers manage payments through the Affirm app

- They receive reminders and payment schedules

- They discover additional merchants through the Affirm marketplace

Stage 4 – Retention

Repeat usage is driven by:

- Positive repayment experiences

- Merchant discovery through the Affirm app

- Consumer trust in transparent pricing

Many users eventually treat Affirm as their default financing option.

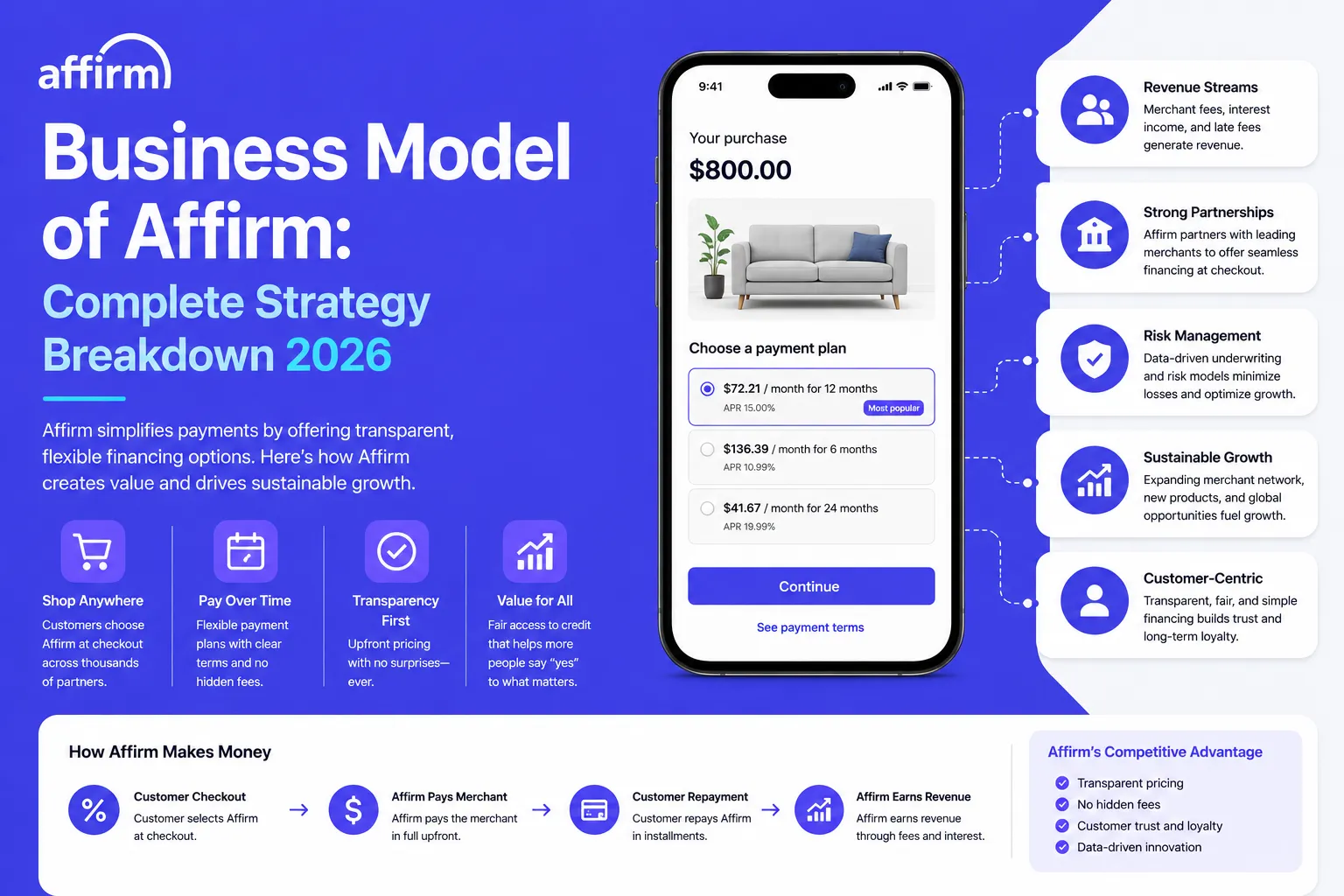

Revenue Streams and Monetization Design

Once Affirm attracts consumers and merchants onto its platform, the next question becomes how money flows through the ecosystem.

Affirm’s monetization strategy is built around transaction-based lending combined with platform economics. Instead of relying solely on interest like traditional lenders, Affirm generates revenue from multiple interconnected streams tied directly to commerce activity.

This diversified revenue architecture allows Affirm to grow revenue alongside merchant sales volume, consumer financing demand, and platform partnerships.

Primary Revenue Stream: Merchant Fees

The largest share of Affirm’s revenue comes from merchant discount fees.

Merchants pay Affirm a percentage of each transaction when a customer chooses Affirm at checkout.

How it works:

- A customer buys a product using Affirm.

- Affirm pays the merchant upfront for the purchase.

- The consumer repays Affirm over time.

- The merchant pays Affirm a fee for enabling the transaction.

Typical merchant fee range:

- 3% – 8% per transaction

Merchants willingly pay this because Affirm directly improves their revenue metrics.

Benefits merchants gain include:

- Higher checkout conversion rates

- Increased average order value

- Reduced cart abandonment

- Access to new customers

In many industries, the revenue lift from financing options outweighs the merchant fee, making Affirm a profitable sales tool rather than just a payment method.

Secondary Revenue Stream: Consumer Interest Payments

Affirm also earns revenue from interest charged on certain loans.

Unlike credit cards, Affirm uses fixed-rate installment loans where the consumer clearly knows the total cost upfront.

Key characteristics:

- Interest rates typically range from 0% to ~30% APR

- Some merchants subsidize 0% financing promotions

- Interest income grows with loan volume

Many consumers prefer this model because there are:

- No compounding interest

- No hidden fees

- No late penalties in most cases

This transparency is a key part of Affirm’s brand identity.

Additional Revenue Streams

1. Interchange Revenue (Affirm Card)

Affirm launched the Affirm Debit+ Card, which generates interchange fees whenever consumers use it for purchases.

Revenue source:

- A percentage of card transaction value paid by payment networks.

This expands Affirm beyond checkout financing into everyday consumer spending.

2. Virtual Card Network Fees

Affirm provides virtual payment cards that allow consumers to finance purchases anywhere.

Revenue includes:

- Transaction processing fees

- Payment network revenue sharing

This helps Affirm expand to merchants without direct integrations.

3. Consumer Marketplace Promotions

Inside the Affirm mobile app, merchants can promote offers to consumers.

These promotional placements function similarly to performance marketing inside a commerce marketplace.

Revenue model:

- Merchant advertising fees

- Featured merchant placements

- Promotion-based commissions

4. Servicing & Platform Fees

Affirm also earns revenue by:

- Servicing loans for funding partners

- Providing underwriting technology

- Managing loan lifecycle operations

Institutional investors and banking partners pay Affirm for these services.

Read more : Affirm Revenue Model: How Affirm Makes Money in 2026

Operational Model & Key Activities

Behind Affirm’s consumer-friendly checkout experience lies a complex operational machine combining fintech infrastructure, data science, risk management, and merchant integrations.

Unlike traditional lenders that rely heavily on manual credit processes, Affirm operates as a technology-first financial platform, where automation, algorithms, and embedded APIs power the majority of operations.

The company’s operational model is designed to approve loans instantly, manage millions of transactions, and balance financial risk in real time.

Core Operations

Affirm’s day-to-day operations revolve around several key functions.

1. Platform Management

Affirm manages the infrastructure that connects:

- Consumers

- Merchants

- Payment networks

- Banking partners

This includes:

- Checkout integrations

- Merchant dashboards

- Consumer mobile apps

- Loan servicing systems

The platform must process millions of payment transactions and credit decisions daily.

2. Credit Underwriting & Risk Management

One of Affirm’s most critical capabilities is its machine-learning credit evaluation system.

Unlike traditional lenders that rely heavily on credit scores alone, Affirm analyzes:

- Transaction history

- Purchase behavior

- Merchant data

- Financial signals

These models allow Affirm to:

- Approve loans instantly

- Predict repayment likelihood

- Adjust credit limits dynamically

- Reduce default risk

This AI-driven underwriting system is one of Affirm’s strongest competitive advantages.

3. Merchant Integration & API Infrastructure

Affirm invests heavily in developer tools and integration systems.

Merchants integrate Affirm through:

- APIs

- Checkout plugins

- E-commerce platform integrations

- Mobile SDKs

Major platform integrations include:

- Shopify

- WooCommerce

- BigCommerce

- Amazon

These integrations allow Affirm to scale across thousands of merchants simultaneously.

For platform development companies like Miracuves, this illustrates how API-first infrastructure enables rapid ecosystem expansion.

4. Loan Servicing & Payment Processing

After a purchase is financed, Affirm manages the entire loan lifecycle.

This includes:

- Payment collection

- Installment scheduling

- Account management

- Fraud detection

- Customer support

Automating these processes allows Affirm to handle millions of repayment schedules simultaneously.

5. Consumer Experience & Support

Consumer trust is central to Affirm’s brand.

Operational teams ensure:

- Clear payment tracking in the mobile app

- Customer service for disputes or account issues

- Notifications and reminders for installments

This focus on transparency strengthens consumer retention and brand loyalty.

Strategic Partnerships & Ecosystem Development

A major reason Affirm scaled rapidly in the fintech ecosystem is its partnership-first strategy. Instead of trying to build every component of the financial stack internally, Affirm designed its model around strategic alliances that expand distribution, funding capacity, and platform reach.

These partnerships allow Affirm to operate simultaneously as a technology platform, payment provider, and lending infrastructure company.

By building a strong ecosystem of partners, Affirm strengthens its network effects — the more merchants and platforms that integrate Affirm, the more valuable the system becomes for consumers and investors.

Technology and API Partners

Technology integrations are the backbone of Affirm’s growth.

Affirm works closely with e-commerce platforms and software providers to embed its financing option directly into online checkout experiences.

Key examples include:

- Shopify – One of Affirm’s most influential partnerships, enabling thousands of Shopify merchants to offer BNPL financing.

- WooCommerce & BigCommerce – Plugins allow small and mid-sized businesses to integrate Affirm quickly.

- Amazon – Affirm powers installment payments for certain purchases on Amazon in the U.S.

- Mobile commerce platforms – SDK integrations for in-app checkout financing.

These integrations ensure Affirm appears exactly at the moment of purchase decision, which dramatically increases adoption.

For companies like Miracuves, this highlights the importance of designing API-first platforms that easily integrate into third-party ecosystems.

Payment and Financial Infrastructure Partnerships

Because Affirm operates within financial services, it collaborates with banks and institutional capital providers to fund loans and manage regulatory requirements.

Key financial ecosystem partners include:

- Banking partners that originate consumer loans

- Institutional investors that purchase loan portfolios

- Payment networks such as Visa and Mastercard

- Credit reporting agencies

These alliances allow Affirm to scale lending capacity without holding all credit risk on its balance sheet.

This hybrid fintech structure combines the agility of a tech platform with the stability of traditional financial institutions.

Merchant and Retail Partnerships

Affirm’s most visible partnerships are with major retail brands and marketplaces.

These collaborations expand Affirm’s consumer reach dramatically.

Notable retail partners include:

- Amazon

- Walmart

- Peloton

- Target merchants through Shopify

- Thousands of direct-to-consumer brands

For merchants, Affirm functions as a growth tool rather than just a payment option.

Retailers benefit from:

- Higher checkout conversions

- Increased order values

- Access to financing for high-ticket purchases

This creates a strong incentive for merchants to promote Affirm during the checkout process.

Marketing and Distribution Alliances

Affirm also collaborates with partners to expand customer acquisition.

Examples include:

- Merchant co-marketing campaigns

- Affiliate partnerships

- Consumer promotions within the Affirm app

- Retail financing promotions during peak shopping seasons

These partnerships turn Affirm into a distribution network for both merchants and financial services.

For companies like Miracuves, this partnership strategy demonstrates how successful digital platforms expand by building ecosystems rather than standalone products.

Platforms that integrate deeply into partner networks often achieve faster scaling and stronger competitive advantages.

Read more : Best Afterpay Clone Scripts 2026: Launch a Powerful BNPL App for Your Fintech Startup

Growth Strategy & Scaling Mechanisms

Affirm’s rapid rise in the fintech ecosystem wasn’t accidental. The company built a multi-layered growth engine combining embedded distribution, merchant partnerships, data-driven underwriting, and product expansion.

Instead of relying solely on traditional marketing, Affirm designed its model so that every transaction fuels future growth.

This strategy turns the platform into a self-reinforcing financial ecosystem where consumer usage, merchant adoption, and loan volume expand together.

Growth Engines

Affirm’s scaling strategy is driven by several key growth mechanisms.

1. Embedded Distribution

One of Affirm’s most powerful growth drivers is checkout integration.

Rather than requiring users to download an app first, Affirm appears directly inside the merchant checkout experience.

When customers see an option like:

“Pay $80/month with Affirm”

it introduces financing exactly at the moment purchasing decisions are made.

This model creates high conversion rates and rapid consumer adoption.

2. Merchant Referral Loop

Merchants play a major role in Affirm’s growth.

When retailers add Affirm as a payment option, they often promote it through:

- Product pages

- Checkout banners

- Email campaigns

- Seasonal promotions

As more merchants integrate Affirm, more consumers encounter the payment option — which in turn encourages additional merchants to join.

This creates a powerful merchant-driven growth loop.

3. Consumer Marketplace App

Affirm also grows through its consumer discovery platform.

The Affirm app allows users to:

- Discover partner merchants

- Browse financing offers

- Manage payments

- Access shopping promotions

This turns Affirm into more than just a payment tool — it becomes a shopping marketplace with embedded financing.

4. Product Expansion

Affirm’s growth strategy also includes expanding into new financial products.

Over time, the company introduced:

- Affirm Debit+ Card

- Savings accounts

- Virtual payment cards

- Merchant analytics tools

Each new product deepens consumer engagement and increases transaction volume across the ecosystem.

5. Geographic Expansion

While Affirm initially focused on the United States, its long-term growth strategy includes international expansion.

Scaling globally requires:

- Regulatory approvals

- Local banking partnerships

- Regional merchant networks

Affirm has gradually expanded into North America and select global markets, positioning itself to compete in the global BNPL sector.

Competitive Strategy & Market Defense

The Buy Now, Pay Later (BNPL) sector has become one of the most competitive segments in fintech. Major players such as Klarna, Afterpay (Block), PayPal Pay Later, and Apple Pay Later have all entered the market, competing for merchants and consumers.

Despite this intense competition, Affirm has maintained a strong position by focusing on technology-driven underwriting, deep merchant integrations, and transparent financial products.

Rather than competing purely on price, Affirm differentiates itself through platform strategy, trust, and financial infrastructure innovation.

Key Competitive Advantages

Affirm’s ability to compete effectively comes from several strategic advantages.

1. Advanced Data & Underwriting Algorithms

One of Affirm’s strongest differentiators is its machine learning credit underwriting system.

Unlike some BNPL competitors that offer simple “pay in four” plans without deep credit evaluation, Affirm analyzes:

- Consumer financial behavior

- Transaction data

- Purchase context

- Merchant history

This allows Affirm to:

- Offer longer-term installment loans

- Approve larger purchase amounts

- Reduce default risk

- Personalize financing offers

This data advantage improves both consumer approval rates and financial stability.

2. Deep Merchant Integrations

Affirm integrates directly into merchant checkout systems through APIs and platform partnerships.

This creates a distribution moat, because once a retailer integrates Affirm, switching to another provider requires:

- Technical changes

- Payment flow adjustments

- Contract renegotiations

Major integrations with platforms like Shopify and Amazon significantly expand Affirm’s reach.

These partnerships ensure Affirm appears exactly where purchasing decisions happen.

3. Brand Trust & Transparent Pricing

Affirm built its brand around financial transparency.

Key differentiators include:

- No hidden fees

- Clear repayment schedules

- Fixed interest rates

- No compounding interest

This messaging resonates strongly with younger consumers who distrust traditional credit card systems.

Over time, this positioning has helped Affirm build consumer trust and long-term brand loyalty.

4. Consumer Ecosystem & App Marketplace

The Affirm consumer app acts as both a payment tool and a shopping discovery platform.

Users can:

- Browse merchants

- Access financing offers

- Track installment payments

- Discover promotions

This creates a closed-loop ecosystem that keeps users engaged with the platform even outside the checkout experience.

Strategic Insight

Affirm’s competitive strategy highlights a key principle of platform businesses:

The strongest competitive advantage often comes from ecosystem integration rather than individual product features.

By combining technology, financial services, merchant partnerships, and consumer trust, Affirm has created a platform that is difficult for competitors to replicate.

For platform builders like Miracuves, this demonstrates how building deep integrations and strong ecosystem relationships can create long-term competitive moats.

Lessons for Entrepreneurs & Implementation

Affirm’s journey offers powerful lessons for founders building fintech platforms, marketplaces, or embedded finance products. Its success wasn’t just about offering installment loans — it was about designing a scalable ecosystem where technology, finance, and commerce intersect.

For entrepreneurs studying Affirm, the real value lies in understanding the principles behind the platform, not just the product itself.

Let’s break down the key takeaways.

Key Factors Behind Affirm’s Success

Several strategic decisions helped Affirm become a major fintech player.

1. Solving a Clear Consumer Pain Point

Traditional credit cards often confuse consumers with:

- Hidden fees

- Compounding interest

- Complex billing structures

Affirm simplified financing with:

- Transparent pricing

- Fixed payment schedules

- Clear total cost visibility

By solving a trust problem in consumer finance, Affirm created strong brand loyalty.

2. Embedding Finance Into Commerce

Rather than building a standalone lending app, Affirm integrated directly into checkout experiences across e-commerce platforms.

This approach allowed the company to scale quickly because:

- Consumers discover Affirm during purchases

- Merchants promote financing options

- Adoption occurs naturally through transactions

Embedded finance is now one of the most powerful trends in digital platforms.

3. Building a Multi-Sided Ecosystem

Affirm didn’t just serve consumers — it built a platform connecting:

- Consumers

- Merchants

- Financial institutions

This multi-sided ecosystem ensures that growth on one side of the platform benefits the others.

For example:

More merchants → more consumers use BNPL

More consumers → more merchants adopt Affirm

This creates a self-reinforcing network effect.

4. Investing Heavily in Data & Technology

Affirm’s machine learning underwriting system enables:

- Faster approvals

- More accurate risk assessment

- Higher transaction volumes

Technology becomes the core asset that powers scalability.

For startups entering fintech, data infrastructure is often more important than the financial product itself.

Implementation Roadmap for Entrepreneurs

Startups looking to build a similar platform should focus on several priorities.

Phase 1: Market Research & Business Model Design

- Identify industries where financing increases conversion.

- Design a sustainable revenue model.

- Build partnerships with financial institutions.

Phase 2: Platform Development

- Build secure payment infrastructure.

- Develop underwriting algorithms.

- Create merchant integration APIs.

This is where companies like Miracuves specialize — building scalable digital platforms that integrate payments, marketplaces, and financial services into a unified ecosystem.

Phase 3: Merchant Acquisition

- Partner with high-transaction merchants.

- Focus on industries with high-ticket purchases.

- Offer incentives for early integrations.

Phase 4: Consumer Growth

- Launch consumer apps and discovery tools.

- Offer promotional financing campaigns.

Use data analytics to personalize financing offers

Ready to implement Affirm’s proven business model for your market?

Miracuves builds scalable platforms with tested business models and growth mechanisms.

With experience supporting many entrepreneurs, Miracuves helps founders design and launch:

- Fintech platforms

- Marketplace ecosystems

- On-demand applications

- Embedded finance solutions

Get your free business model consultation today and start building your next scalable platform.

Conclusion

Affirm’s business model proves that innovation in financial services doesn’t always mean inventing new products — sometimes it means redesigning how existing services are delivered.

By embedding financing directly into the checkout experience, Affirm transformed a traditional lending product into a seamless commerce infrastructure layer. The company aligned the interests of consumers, merchants, and capital partners, creating a platform where every transaction strengthens the ecosystem.

Its success demonstrates a powerful lesson for modern founders: the future of fintech lies in embedded finance, transparent pricing, and ecosystem-driven platforms..For entrepreneurs and innovators, the real opportunity lies in identifying where financial friction exists in everyday transactions — and designing platforms that remove it.

The platform economy is only accelerating, and the next generation of startups will likely build on the same principle that powered Affirm’s growth: Make financial services invisible, integrated, and intelligent.

FAQs

What type of business model does Affirm use?

Affirm operates a hybrid fintech platform model combining Buy Now Pay Later (BNPL), embedded finance, and marketplace economics. It connects consumers, merchants, and financial partners through installment financing integrated directly into checkout experiences.

How does Affirm’s model create value?

Affirm creates value by enabling flexible installment payments for consumers while increasing conversion rates and order value for merchants. This win-win dynamic drives transaction growth and platform adoption.

What are Affirm’s key success factors?

Affirm’s success comes from transparent pricing, strong merchant partnerships, advanced credit underwriting technology, and embedded checkout integrations. These elements help it scale across both consumers and retailers.

How scalable is the Affirm business model?

The model is highly scalable because it relies on platform integrations, APIs, and financial partnerships rather than physical infrastructure. As more merchants join the ecosystem, consumer adoption grows automatically.

What are the biggest challenges for Affirm?

Major challenges include credit risk management, regulatory scrutiny, and intense competition from other BNPL providers. Managing loan performance while expanding globally remains a critical balancing act.

How can entrepreneurs adapt the Affirm model to their region?

Entrepreneurs can adapt the model by offering installment payments for high-value products or services in their local markets, such as healthcare, education, travel, or electronics.

What are alternatives to the Affirm business model?

Alternative models include subscription-based fintech platforms, traditional credit card lending, peer-to-peer lending marketplaces, and digital wallets with integrated financing.

How has Affirm’s business model evolved over time?

Affirm began as a consumer installment loan provider but evolved into a broader fintech ecosystem including debit cards, merchant tools, savings products, and a consumer shopping marketplace.

Related Articles