Key Takeaways

What You’ll Learn

- Plaid connects financial institutions with fintech apps through secure APIs.

- The company earns revenue mainly from API usage and fintech integrations.

- Plaid powers banking connectivity for apps like payments, investing, and budgeting platforms.

- Its infrastructure helps fintech companies launch faster without building banking systems from scratch.

- Data connectivity and financial automation are central to Plaid’s long-term growth strategy.

Stats That Matter

- Plaid connects more than 10,000 financial institutions and fintech applications globally.

- One in two Americans has reportedly used Plaid-powered banking connectivity.

- Plaid’s annual recurring revenue surpassed $500 million with continued fintech expansion.

- The global open banking market continues growing as digital finance adoption increases.

- API-driven fintech infrastructure is becoming essential for modern financial applications.

Real Insights

- Fintech growth depends heavily on secure and reliable banking infrastructure.

- Platforms like Plaid reduce development complexity for startups and fintech companies.

- Open banking APIs are reshaping how users connect and manage financial services.

- Trust, compliance, and data security remain critical in financial technology platforms.

- Infrastructure-focused fintech businesses can scale rapidly by serving multiple apps and industries.

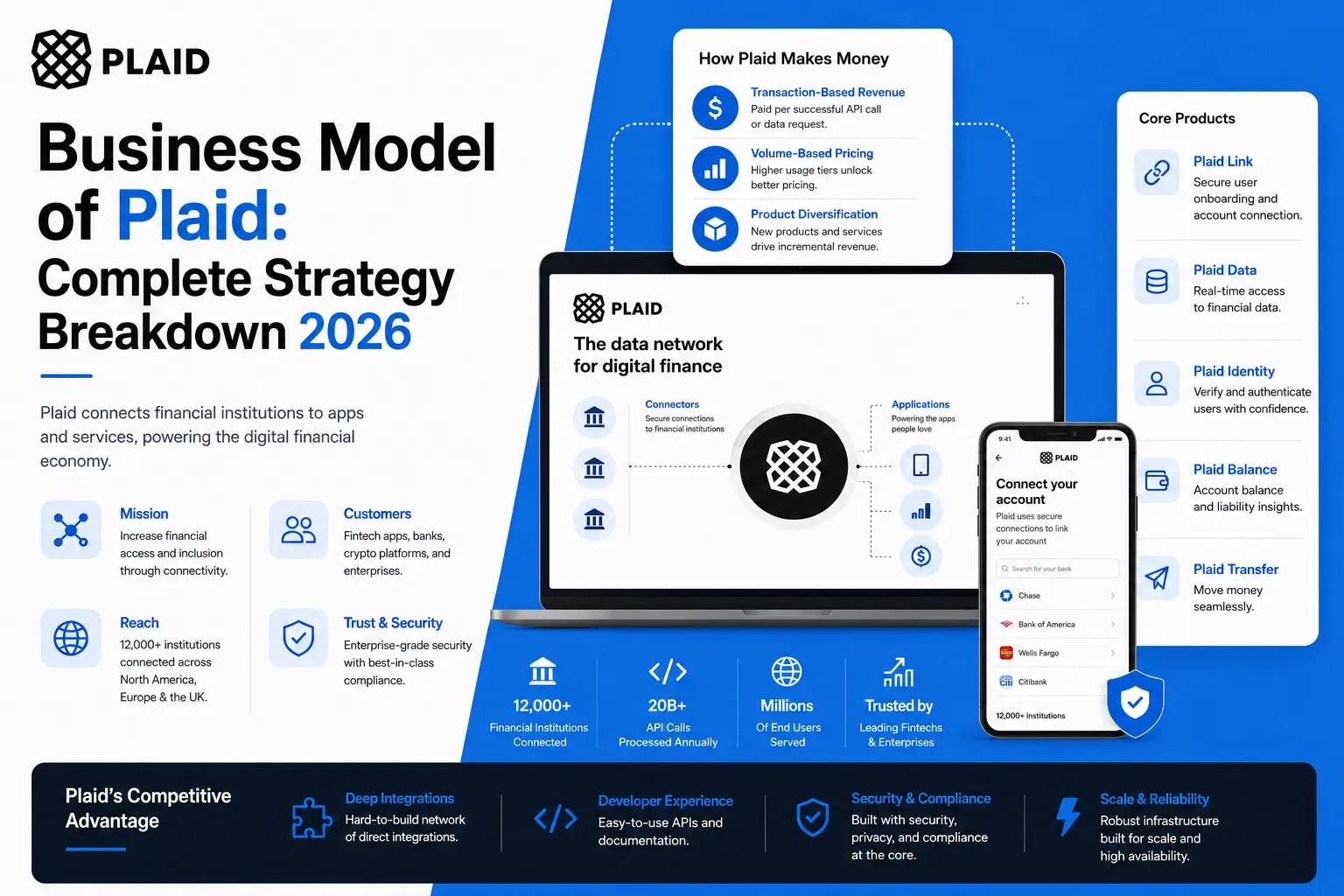

Plaid grew from a small fintech startup into a $13+ billion infrastructure giant, powering over 8,000 apps including Venmo, Robinhood, and Coinbase — without ever being a consumer-facing brand. If fintech apps are the “front-end experience,” Plaid is the invisible engine underneath.

Founded in 2013, Plaid didn’t try to compete with banks — it connected them to the future. By enabling secure data sharing between financial institutions and apps, Plaid became the backbone of the modern digital finance ecosystem.

In 2026, as open banking, embedded finance, and API-driven ecosystems dominate, Business Model of Plaidis more relevant than ever. For entrepreneurs, understanding Plaid isn’t just useful — it’s essential if you’re building: Fintech apps, neobanks, payment platforms, and lending or investment products are all digital financial solutions that leverage technology to deliver faster, more accessible, and user-centric financial services.At Miracuves, we see a growing trend: founders no longer build full financial systems — they build on top of platforms like Plaid to scale faster and smarter.

How the Plaid Business Model Works

Plaid operates as a financial data infrastructure platform, sitting between banks and applications. It enables apps to securely access user-permissioned financial data through APIs — making it a foundational layer of the fintech ecosystem.

Instead of serving end-users directly, Plaid powers the experiences of other apps — a classic example of a B2B2C platform model.

Type of Business Model

Plaid uses a Hybrid API + Usage-Based SaaS Model:

- API Platform → Developers integrate Plaid to access financial data

- Usage-Based Pricing → Clients pay based on API calls, active users, or products used

- Infrastructure-as-a-Service (IaaS for Fintech)

Value Proposition

Plaid creates value for multiple stakeholders:

For Developers / Fintech Companies

- Instant access to bank data (accounts, transactions, identity)

- Faster product development (weeks instead of months)

- Regulatory and compliance simplification

For Consumers

- Seamless bank linking experience (e.g., connecting bank to apps in seconds)

- Secure, permission-based data sharing

For Financial Institutions

- Access to modern fintech ecosystems

Increased transaction volume and engagement

Evolution of the Model

Plaid’s model has significantly evolved:

- 2013–2016: Focus on bank connectivity (basic API layer)

- 2017–2020: Expansion into transactions, identity, and authentication

- 2021–2024: Growth into payments, fraud detection, and open finance

- 2025–2026: Shift toward embedded finance infrastructure + global expansion

Today, Plaid is not just a connector — it’s a financial data network with multiple monetizable layers.

Why It Works in 2026

Plaid thrives due to major market shifts:

- Open Banking Regulations (EU, UK, India emerging frameworks)

- Rise of embedded finance (non-fintech apps offering financial features)

- Demand for real-time financial data

Read more : What Is Plaid and How Does It Work?

Target Market & Customer Segmentation Strategy

Plaid’s strength lies in targeting developers and fintech companies first, not consumers — a strategic move that allows it to scale invisibly while powering millions of end users globally.

Its segmentation strategy is deeply rooted in ecosystem thinking, where each customer group amplifies the value of the others.

Primary Customer Segments

1. Fintech Startups & Scaleups

- Neobanks (e.g., Chime)

- Investment apps (e.g., Robinhood)

- Crypto platforms (e.g., Coinbase)

- Lending & credit apps

Behavior:

- Need fast go-to-market

- Prefer plug-and-play APIs over building infrastructure

- Highly sensitive to developer experience and uptime

2. Enterprises & Financial Institutions

- Traditional banks integrating digital capabilities

- Large fintech platforms expanding services

- Payment companies

Behavior:

- Focus on compliance, reliability, and scalability

- Require custom integrations and enterprise-grade support

Secondary Customer Segments

3. Developers (Key Influencers)

- Independent developers or engineering teams

- Often the decision-makers in choosing Plaid

Behavior:

- Value documentation, SDKs, and sandbox environments

- Prefer tools that reduce complexity

4. End Users (Indirect Segment)

- Consumers using apps powered by Plaid

Behavior:

- Expect seamless onboarding (bank linking in seconds)

- Prioritize trust and security

Customer Journey Mapping

Plaid’s growth engine is built around a developer-first journey:

1. Discovery

- Developer communities

- Word-of-mouth in fintech ecosystem

- Documentation & case studies

2. Evaluation

- Sandbox testing

- API documentation

- Integration ease

3. Conversion

- Quick API integration

- Transparent pricing tiers

4. Retention

- High switching costs once integrated

Continuous product expansion (identity, payments, fraud tools)

Revenue Streams and Monetization Design

Now that we understand who Plaid serves, the next question is:

How does Plaid actually make money?

Plaid’s monetization is built on a layered, usage-driven revenue architecture, where clients pay more as they grow — aligning Plaid’s success directly with its customers’ success.

Primary Revenue Stream: API Usage Fees

This is the core engine of Plaid’s business.

How it works:

- Clients pay based on:

- Number of connected users (accounts linked)

- API calls (data requests)

- Product usage (transactions, identity, assets, etc.)

- Number of connected users (accounts linked)

Pricing Model:

- Pay-as-you-go + volume-based tiers

- Custom enterprise pricing for large clients

Revenue Contribution:

- Estimated 60–70% of total revenue

Growth Trajectory:

- Scales automatically as:

- Fintech apps grow users

- More features are integrated

- Fintech apps grow users

Example:

- A budgeting app pays per connected bank account

- A lending app pays for transaction history + identity verification

Secondary Revenue Streams

1. Premium Products (Data & Insights APIs)

Plaid monetizes advanced capabilities beyond basic connectivity:

- Transaction categorization

- Income verification

- Risk and fraud signals

Contribution: ~15–20%

Strategy: Upsell high-value data services to existing clients

2. Identity & KYC Solutions

With rising compliance needs, Plaid expanded into:

- Identity verification

- AML/KYC compliance tools

Contribution: Growing rapidly in 2025–2026

Why it matters: Regulatory tech = high-margin revenue

3. Payments & Transfer Services

Plaid enables:

- ACH payments

- Account-to-account transfers

Revenue Model:

- Per transaction fee

- Value-added services (instant transfers, fraud protection)

Contribution: ~10–15% and increasing

4. Data Analytics & Insights for Enterprises

Plaid provides aggregated, anonymized insights:

- Consumer spending patterns

- Financial behavior trends

Used by:

- Banks

- Lenders

- Enterprise fintech firms

5. International Expansion Revenue

With growth in:

- Europe (PSD2 open banking)

- India (Account Aggregator framework)

- LATAM emerging fintech markets

Plaid generates revenue through:

- Regional pricing models

- Local partnerships

Read more : Plaid Revenue Model: How Plaid Makes Money in 2026

Operational Model & Key Activities

Behind Plaid’s seamless API experience lies a highly sophisticated operational engine — one that balances data security, uptime reliability, compliance, and developer usability at scale.

Unlike consumer apps, Plaid’s operations are invisible — but mission-critical.

Core Operations

Plaid’s day-to-day business revolves around maintaining a high-performance financial data network:

1. Platform & API Management

- Ensuring APIs are stable, fast, and scalable

- Continuous updates to support new financial institutions

- Maintaining SDKs and developer tools

2. Data Infrastructure & Connectivity

- Securely connecting with 12,000+ financial institutions globally

- Handling massive volumes of real-time financial data

- Ensuring data normalization across different banking systems

3. Security & Compliance

- End-to-end encryption and tokenization

- Compliance with:

- GDPR (Europe)

- SOC 2 standards

- Open banking regulations

- GDPR (Europe)

Trust is Plaid’s biggest asset — a single failure could impact thousands of apps.

4. Product Development & Innovation

- Expanding APIs into:

- Payments

- Identity

- Fraud detection

- Payments

- Continuous iteration based on developer feedback

5. Customer Support & Developer Success

- Dedicated support teams for enterprise clients

- Developer documentation, sandbox environments

- Integration troubleshooting

Strategic Partnerships & Ecosystem Development

Plaid’s growth isn’t just driven by technology — it’s powered by a carefully orchestrated ecosystem of partnerships.

Instead of building everything in-house, Plaid acts as a connective layer, collaborating with banks, fintechs, and infrastructure providers to create a unified financial network.

Collaboration Philosophy

Plaid follows a “platform-first, ecosystem-always” approach:

“Win by enabling others to win.”

This means:

- Empower fintech startups to launch faster

- Help banks modernize without rebuilding systems

- Create mutual value across the ecosystem

Key Partnership Types

1. Technology & API Partners

- Cloud providers (AWS, Google Cloud)

- Developer tools and fintech infrastructure platforms

Role:

- Ensure scalability, uptime, and seamless integrations

- Expand Plaid’s capabilities through APIs

2. Financial Institutions & Banking Partners

- Traditional banks and credit unions

- Digital-first banks

Role:

- Provide access to financial data

- Enable secure data-sharing frameworks

This is the foundation of Plaid’s entire model

3. Payment & Transfer Alliances

- ACH networks

- Payment processors and gateways

Role:

- Enable account-to-account payments

- Improve transaction speed and reliability

4. Fintech & App Ecosystem Partners

- Apps like Venmo, Robinhood, Coinbase, Chime

Role:

- Drive demand for Plaid APIs

- Expand usage and revenue through integration

These partners are also Plaid’s biggest growth drivers

5. Regulatory & Expansion Alliances

- Open banking regulators (EU PSD2 ecosystem)

- India’s Account Aggregator framework participants

- Regional compliance partners

Role:

- Ensure legal operation in global markets

Enable faster geographic expansion

Growth Strategy & Scaling Mechanisms

Plaid’s growth story is a masterclass in invisible scaling — it didn’t grow by acquiring users directly, but by becoming essential to the apps that do.

Instead of chasing consumers, Plaid focused on embedding itself into the fintech ecosystem, allowing growth to compound naturally.

Growth Engines

1. Organic Virality (Developer-Led Growth)

Plaid spreads through the developer community:

- Developers recommend Plaid to other developers

- Popular apps using Plaid validate its reliability

- Integration success stories drive adoption

- This creates a silent but powerful viral loop

2. Ecosystem-Driven Referrals

- When a fintech app scales, Plaid scales with it

- New startups copy successful apps → adopt same infrastructure

Example:

- A new neobank sees Chime’s stack → integrates Plaid

Growth becomes industry-standard adoption

3. Paid Enterprise Expansion

Plaid complements organic growth with:

- Enterprise sales teams targeting banks and large fintechs

- Strategic account expansion within existing clients

Focus: fewer clients, higher value

4. Product-Led Expansion

Plaid grows by adding more products:

- Start: Account linking

- Expand: Transactions, identity, payments, fraud

Each new product increases:

- Revenue per client

- Platform dependency

5. Geographic Expansion

Plaid’s 2025–2026 expansion strategy includes:

- Europe (leveraging PSD2 open banking)

- India (Account Aggregator ecosystem)

- LATAM (rapid fintech adoption)

Approach:

- Local partnerships

- Regulatory-first entry

Competitive Strategy & Market Defense

Plaid operates in one of the most competitive and rapidly evolving sectors — fintech infrastructure. Yet, despite growing competition from banks, open banking APIs, and new startups, Plaid has maintained a dominant position.

Its advantage lies not in a single feature — but in a layered competitive strategy.

Core Competitive Advantages

1. Network Effects & Switching Barriers

Plaid’s biggest strength is its deep integration network:

- Connected to thousands of financial institutions

- Embedded in 8,000+ apps

- Powers millions of user connections daily

The more apps use Plaid, the harder it becomes to replace it.

Switching Challenge:

- Replacing Plaid requires:

- Rebuilding integrations

- Migrating user connections

- Ensuring zero downtime

- Rebuilding integrations

Result: Extremely high switching costs

2. Brand Equity & Developer Trust

Plaid is not a consumer brand — but in fintech, it’s a trusted standard.

- Known for reliability and security

- Widely recommended in developer communities

- Backed by strong case studies (Venmo, Robinhood, Coinbase)

Trust = adoption = retention

3. Superior Developer Experience

Plaid wins by being easy to use:

- Clean APIs

- Excellent documentation

- Sandbox environments for testing

Developers choose Plaid because it reduces friction

4. Data Advantage & Personalization

Plaid processes massive volumes of financial data:

- Enables better categorization and insights

- Powers smarter financial decisions in apps

Over time, this creates a data-driven moat

5. Continuous Innovation

Plaid consistently expands its offerings:

- From data access → payments → identity → fraud detection

- Adapting to trends like:

- Embedded finance

- AI-driven financial tools

- Embedded finance

Lessons for Entrepreneurs & Implementation

Business Model of Plaid journey offers more than just inspiration — it provides a blueprint for building scalable, high-impact platform businesses.

If you’re a founder in 2026, especially in fintech or digital ecosystems, there are clear, actionable lessons you can apply immediately.

Key Factors Behind Plaid’s Success

1. Infrastructure Over Interface

- Plaid didn’t build a flashy consumer app

- It built the foundation others rely on

Result: Less competition, deeper integration, higher retention

2. Developer-First Approach

- Prioritized APIs, documentation, and ease of use

- Turned developers into growth drivers

Developers became advocates + distribution channel

3. Multi-Layer Monetization

- Started with basic APIs

- Expanded into identity, payments, and analytics

Revenue grows as customers grow

4. Ecosystem Thinking

- Connected banks, apps, and users

- Created value for all participants

Network effects drive long-term dominance

5. Trust as a Core Asset

- Invested heavily in security and compliance

- Built credibility in a sensitive domain (finance)

Trust = adoption + scalability

Replicable Principles for Startups

Here’s how you can apply Plaid’s strategy:

1. Start with a Core Pain Point

- Identify a universal infrastructure gap

- Solve it better than anyone else

2. Build for Builders

- Target developers, businesses, or creators first

- Let them bring users to you

3. Use Usage-Based Pricing

- Lower entry barrier

- Align pricing with customer growth

4. Expand Horizontally

- Start with one product

- Gradually add complementary services

5. Design for Lock-In (Ethically)

- Build deep integrations

- Make your product indispensable

Implementation Timeline & Investment Priorities

Phase 1: Foundation

- Identify niche infrastructure gap

- Build MVP API product

- Focus on developer usability

Phase 2: Validation

- Acquire early B2B clients

- Refine product based on feedback

- Strengthen security & reliability

Phase 3: Expansion

- Add new product layers

- Scale partnerships

- Introduce usage-based monetization

Phase 4: Scale

- Expand geographically

- Build ecosystem integrations

- Optimize revenue streams

Ready to implement Plaid’s proven business model for your market?

Miracuves builds scalable platforms with tested business models and growth mechanisms.

Get your free business model consultation today.

Conclusion

Plaid’s business model proves a powerful point: You don’t need to own the customer to own the market.

By positioning itself as the infrastructure layer of fintech, Plaid transformed from a simple API provider into a critical backbone of the global financial ecosystem. It didn’t compete with banks or apps — it enabled both, and in doing so, became indispensable. Its success is not just about technology, but about: Strategic positioning , Ecosystem thinking ,Scalable monetization , Relentless focus on trust and reliability

For entrepreneurs, the bigger lesson is clear:

The future belongs to platforms that enable others to build, grow, and scale.

As we move deeper into 2026 and beyond, platform economies will continue to dominate — especially those built on: Open ecosystems , API-first architecture , Data-driven intelligence

And companies like Plaid will remain at the center of this transformation — quietly powering the next generation of billion-dollar businesses.

FAQs

What type of business model does Plaid use?

Plaid uses a B2B2C API-based platform model with usage-based SaaS pricing. It provides financial data infrastructure to apps that serve end users.

How does Plaid’s model create value?

It simplifies secure access to financial data, reducing development time for apps while improving user experience. This creates value for developers, businesses, and consumers simultaneously.

What are its key success factors?

Strong developer experience, deep bank integrations, high trust in security, and scalable API infrastructure are the main drivers of Plaid’s success.

How scalable is it?

Extremely scalable — Plaid grows as its clients grow. Since it’s API-based, it can expand globally without directly acquiring users.

What are the biggest challenges?

Regulatory compliance, maintaining data security, and handling complex bank integrations across regions are major challenges

How can entrepreneurs adapt it to their region?

Focus on local regulations, build partnerships with regional institutions, and create APIs that solve specific industry or geographic problems.

What are alternatives to this model?

Alternatives include direct-to-consumer fintech apps, traditional SaaS platforms, or fully integrated banking solutions without open APIs.

How has it evolved over time?

Plaid evolved from a simple bank connectivity tool to a full financial infrastructure platform offering payments, identity, and data analytics services

Related Articles

- Best Nubank Clone Scripts 2025: Build the Future of Digital Banking

- Best Razorpay Clone Scripts 2025: Build Your Own Payment Gateway Platform

- Best Wealthfront Clone Scripts 2025: Launch Your Automated Investing Platform Faster

- What is Affirm and How Does It Work?

- What is Afterpay and How Does It Work?