Key Takeaways

What You’ll Learn

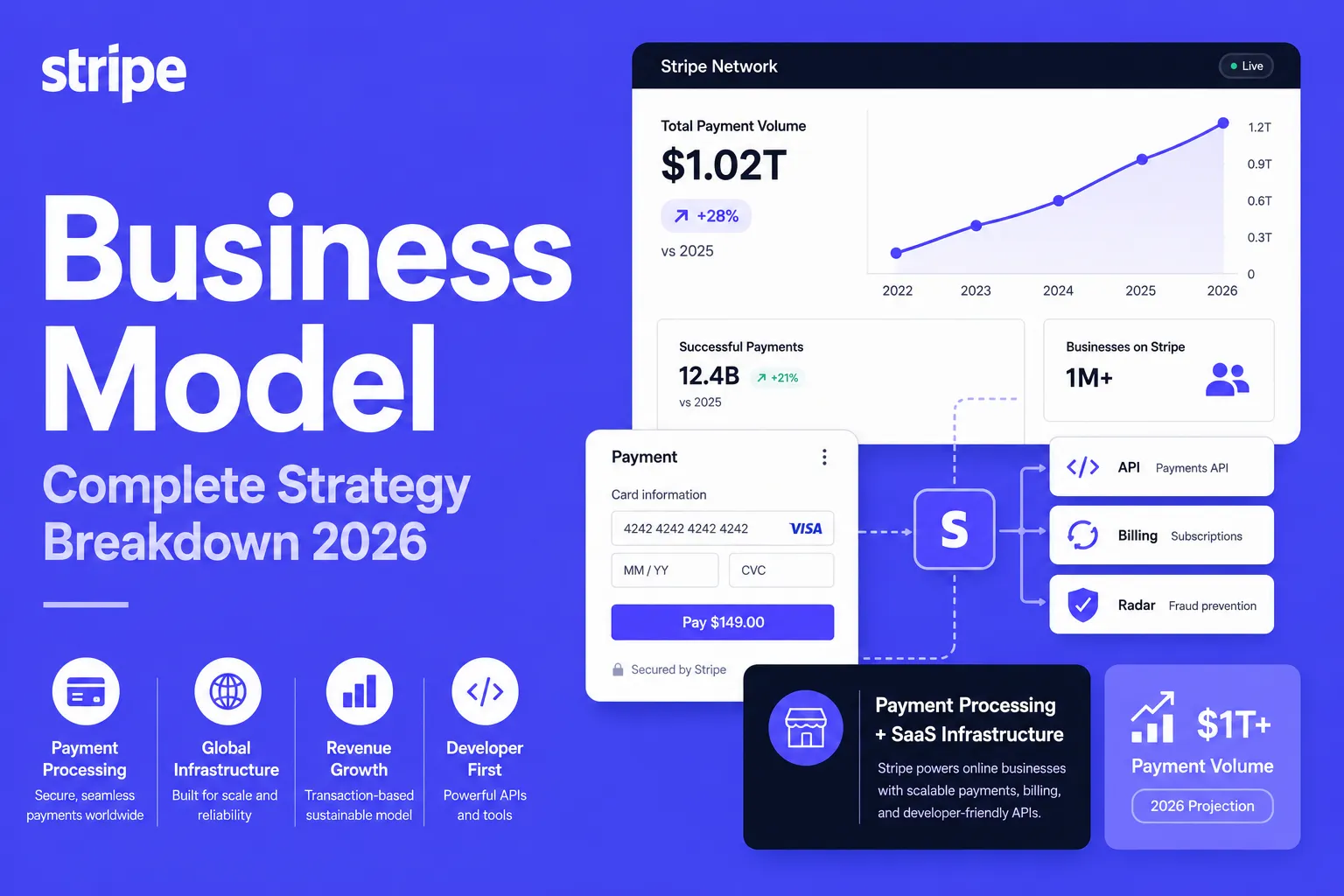

- Stripe’s business model is built around payment infrastructure that helps businesses accept online payments, manage transactions, automate billing, and expand globally.

- The company earns mainly through transaction-based fees charged on card payments, payment processing, international transactions, currency conversion, and value-added financial tools.

- Developer-friendly APIs are Stripe’s biggest advantage because startups, SaaS companies, marketplaces, and enterprises can integrate payments quickly without building financial infrastructure from scratch.

- Stripe expands revenue through multiple product layers including Billing, Connect, Radar, Tax, Terminal, Atlas, Issuing, Treasury, and enterprise payment solutions.

- The biggest takeaway for founders is that Stripe succeeds by turning complex financial operations into simple, scalable, API-first infrastructure for modern businesses.

Stats That Matter

- The article positions Stripe as a global fintech infrastructure company serving startups, SaaS platforms, marketplaces, eCommerce brands, subscription businesses, and large enterprises.

- Core revenue comes from payment processing fees where Stripe charges businesses for successful card payments, online transactions, and payment method handling.

- Stripe Connect supports marketplace monetization by helping platforms manage sellers, payouts, onboarding, compliance, and split payments at scale.

- Stripe Billing and Tax create recurring revenue support for SaaS companies through subscription management, invoicing, usage-based billing, tax calculation, and payment recovery workflows.

- Additional monetization comes from fraud prevention, in-person payments, card issuing, treasury tools, currency conversion, and enterprise-grade financial infrastructure.

Real Insights

- Stripe succeeds because it removes payment complexity for businesses by handling checkout, compliance, payouts, fraud prevention, subscriptions, and global payment methods through one platform.

- The API-first approach makes Stripe deeply embedded because once businesses build around Stripe’s payment logic, switching becomes more difficult as transaction volume grows.

- Its strongest revenue advantage is product expansion where a business may start with payments and later adopt billing, tax, fraud tools, marketplace payouts, issuing, and treasury products.

- Global scale increases Stripe’s platform value because businesses need multi-currency support, local payment methods, regulatory coverage, and reliable settlement infrastructure.

- For entrepreneurs, the biggest lesson is to build a Stripe-style fintech platform around payment processing, developer APIs, compliance automation, fraud control, marketplace payouts, and scalable financial infrastructure.

Stripe started as a simple developer-first payment tool, but today it powers a massive share of global online commerce. The Business Model of Stripe matters in 2026 because it shows how a platform can quietly become the financial infrastructure behind thousands of apps, marketplaces, and SaaS products. From startups to enterprise brands, Stripe wins by making complex payments feel simple, fast, and reliable.

At its core, the Business Model Stripe is built on enabling businesses to accept, move, and manage money across channels and countries. It combines payment processing, billing, fraud prevention, payouts, and embedded finance into one ecosystem. This “API-first” approach creates strong retention because once Stripe is integrated, switching becomes expensive and risky for most companies.

What makes the Stripe powerful is how it scales with customer growth. As merchants increase transactions, subscriptions, and international expansion, Stripe’s revenue grows automatically. For entrepreneurs, Stripe is a masterclass in building a product-led platform, creating trust through reliability, and monetizing at every layer of the digital economy.

How the Stripe Business Model Works

Stripe is not “just a payment gateway.” It is a full-stack financial infrastructure platform that helps businesses accept payments, manage subscriptions, prevent fraud, send payouts, and launch embedded finance products—all through APIs. In simple terms, Stripe sits between customers, banks, card networks, and businesses, and makes money by powering the transaction flow and value-added financial services.

1) Type of Model (2026)

Stripe runs a Hybrid Platform Model, combining:

- B2B Payments Infrastructure (core engine)

- Usage-based SaaS (billing, fraud, data tools)

- Fintech + Embedded Finance (issuing, treasury, lending partnerships)

- Ecosystem Platform (apps, partners, integrations)

2) Stripe’s Value Proposition (By User Segment)

Stripe succeeds because it gives each stakeholder a clear benefit:

For Businesses (Merchants / Platforms)

- Fast setup + developer-friendly APIs

- Global payment acceptance + local methods

- Higher conversion via optimized checkout

- Compliance, security, fraud handling built-in

For Developers & Product Teams

- Clean documentation + stable infrastructure

- Quick integrations + modular products

- Tools to scale from MVP → enterprise

For Marketplaces & Platforms

- Split payments, onboarding, KYC support

- Multi-party payouts and escrow-like flows

- Built for complex payment routing

For Enterprise Companies

- High uptime + reliability

- Custom pricing, risk controls, reporting

- Global expansion support

3) Key Stakeholders in the Stripe Ecosystem

Stripe’s ecosystem stays balanced because each participant plays a role:

- Customers (buyers): pay via card, wallet, bank transfer, BNPL

- Merchants (businesses): accept payments + manage revenue flows

- Stripe: processes payments + manages risk + provides tools

- Banks & Card Networks: enable settlement and authorization

- Partners (apps/tools): extend Stripe’s value via integrations

- Regulators: influence compliance, KYC/AML, data handling

4) How Stripe’s Model Evolved Over Time

Stripe expanded beyond payments because payments alone become commoditized.

- Phase 1: Simple online card payments for startups

- Phase 2: Billing + subscriptions + recurring revenue tools

- Phase 3: Marketplace infrastructure (Connect) + global scale

- Phase 4: Embedded finance products (Issuing, Treasury-like tools)

- Phase 5 (2026): Full revenue operating system (payments + finance + automation)

5) Why Stripe Works Even Better in 2026

Stripe fits modern business behavior in 2026 because:

- More businesses sell globally from day one

- Subscription + usage-based pricing is mainstream

- Marketplaces and multi-vendor platforms keep growing

- Fraud + compliance complexity keeps increasing

- Companies prefer “plug-and-play” infrastructure over building from scratch

Read more : What is Stripe and How Does It Work?

Target Market & Customer Segmentation Strategy

Stripe’s growth is powered by one smart positioning move: it doesn’t target “everyone.” It targets internet businesses that want to move money faster, safer, and globally—without building a banking-grade system internally. In 2026, Stripe serves a wide spectrum of companies, but the core customer mindset stays the same: “We want to scale revenue operations with minimal friction.”

1) Primary & Secondary Customer Segments

Stripe’s customer base can be understood in layers:

Primary Segments

- Startups & SMBs (digital-first): SaaS, ecommerce, D2C brands, creators

- Mid-market scaleups: fast-growing subscription businesses and marketplaces

- Marketplaces & platforms: multi-vendor businesses needing split payments + payouts

Secondary Segments

- Enterprise brands: global companies modernizing payments + billing

- Fintechs: building financial products using Stripe’s infrastructure

- B2B service providers: agencies, logistics, education platforms, travel, etc.

2) Customer Journey: Discovery → Conversion → Retention

Stripe’s funnel is strong because it is product-led.

Discovery

- Developers find Stripe via documentation, tutorials, GitHub, community content

- Founders discover it through startup ecosystems and platform recommendations

Conversion

- Quick signup + sandbox testing

- “First payment success” becomes the activation moment

- Modular add-ons (Billing, Radar, Connect) increase early adoption

Retention

- Deep integration into checkout + billing flows

- Trust built through uptime, fraud handling, and compliance support

- Expansion happens naturally as business volume grows

3) Acquisition Channels & How LTV is Optimized

Stripe doesn’t rely on one marketing channel. It scales through a mix of trust + distribution.

- Product-led growth (PLG): developers adopt first, business expands later

- Partner ecosystem: ecommerce platforms, SaaS tools, marketplaces

- Enterprise sales: custom deals for high-volume merchants

- Content + education: guides, case studies, integration playbooks

LTV optimization happens through:

- Increasing transaction volume over time

- Cross-selling add-ons (Billing, Radar, Connect, Issuing)

- International expansion support (new payment methods + currencies)

4) Market Positioning

Stripe’s competitive edge is its brand voice: developer-first + enterprise-ready.

It differentiates through speed of integration, global reliability, and a “platform layer” approach where businesses can build custom finance workflows without rebuilding the infrastructure.

Revenue Streams and Monetization Design

Once you understand who Stripe serves, the next question becomes obvious: how does Stripe actually make money?

The Business Model of Stripe is designed like a layered monetization engine. Stripe earns revenue from core payment processing, but the real strength is how it expands revenue per customer through billing, fraud tools, marketplace payouts, and embedded finance products. This creates a compounding model where Stripe’s income grows as customers scale.

Primary Revenue Stream 1: Payment Processing Fees (Core Engine)

Mechanism

Stripe charges businesses a fee every time a payment is successfully processed. This includes card payments, wallets, and local payment methods.

Pricing Model (2026)

- Per-transaction fee structure (fixed + %)

- Higher value for:

- international cards

- currency conversion

- advanced routing/optimization

- international cards

Revenue Contribution

- Largest revenue driver for Stripe globally

- Scales automatically with merchant GMV (payment volume)

Growth Trajectory (2026)

- More global ecommerce and SaaS payments

- Higher share of recurring + subscription payments

- Strong adoption of optimized checkout experiences

Secondary Revenue Stream 2: Stripe Billing (Subscriptions + Recurring Revenue)

Mechanism

Stripe monetizes recurring businesses by powering:

- subscription plans

- invoicing

- renewals, proration, upgrades/downgrades

- failed payment recovery

Why it prints revenue

- Billing becomes “sticky” because it touches revenue logic + customer lifecycle

Secondary Revenue Stream 3: Stripe Connect (Marketplaces & Platforms)

Mechanism

Stripe earns from platforms that need:

- onboarding sellers/providers

- split payments

- automated payouts

- compliance workflows (KYC/AML)

Why it’s powerful

- Multi-party payment flows create higher complexity → higher platform value

- Stripe becomes infrastructure for marketplace economies

Secondary Revenue Stream 4: Fraud Prevention & Risk Tools (Stripe Radar)

Mechanism

Stripe charges for enhanced fraud detection, risk scoring, and dispute tools.

Value to customers

- reduces chargebacks

- protects conversion rates

- improves approval rates without increasing fraud

Secondary Revenue Stream 5: Embedded Finance (Issuing + Treasury-like Capabilities)

Mechanism

Stripe enables businesses to launch fintech-style products like:

- branded cards (Issuing)

- stored balances and payouts

- financial workflows via APIs

Why it expands monetization

- Stripe earns through usage-based financial services layered on top of payments

Overall Monetization Strategy (What Makes It Work)

Stripe’s revenue strategy works because each product strengthens the next:

- Payments bring customers in

- Billing increases retention + recurring revenue control

- Connect unlocks marketplace scale

- Radar protects margins by reducing fraud loss

- Embedded finance increases revenue per customer over time

The psychology behind Stripe’s pricing is simple: low friction to start, then monetize deeper as the business becomes more complex and higher volume.

Operational Model & Key Activities

Stripe’s business looks simple from the outside—“process payments”—but operationally it runs like a high-availability financial system. In 2026, Stripe’s real advantage is not only product design, but how smoothly it executes payments, compliance, risk control, and uptime at global scale. This is the machine that keeps merchants trusting Stripe with their revenue every day.

1) Core Operations (What Stripe Does Daily)

Platform Management

- Maintaining global payment routing and settlement flows

- Ensuring high uptime and fast transaction processing

- Monitoring transaction failures, latency, and system reliability

Tech Infrastructure

- API stability + versioning support for long-term integrations

- Data security, encryption, tokenization, and fraud monitoring

- Payment orchestration across banks, networks, and local rails

Quality Control & Risk Management

- Fraud detection and dispute handling workflows

- Compliance monitoring (KYC, AML, regional regulations)

- Risk scoring for merchants and transaction patterns

Customer Support & Merchant Success

- Support for developers, startups, and enterprise teams

- Documentation updates and onboarding improvements

- Incident response + transparency reporting during outages

Marketing & Growth Ops

- Product-led growth through developer ecosystems

- Partner enablement (platforms, SaaS tools, agencies)

- Enterprise sales support for large-volume merchants

2) Resource Allocation (Where Stripe Invests in 2026)

Stripe’s spending priorities are aligned with one mission: trust + scale.

- Tech & Infrastructure: heavy investment in uptime, reliability, global routing

- Security & Compliance: constant upgrades for fraud, AML, regulatory readiness

- R&D / Product Expansion: building new finance modules (billing, issuing, automation)

- Enterprise Enablement: account management, custom integrations, SLAs

- Global Expansion: adding local payment methods and region-specific compliance

3) What This Means for Founders

Stripe proves a key platform lesson: operations is the product.

In fintech infrastructure, users don’t just pay for features—they pay for reliability, security, and predictable execution. That’s why Stripe becomes hard to replace once integrated. This is also where Miracuves adds value for founders building platforms: we focus on scalable architecture, secure payment-ready flows, and marketplace-grade operational design so your app can grow without breaking.

Strategic Partnerships & Ecosystem Development

Stripe didn’t scale into a global payments leader by building everything alone. Its real strength is partnership thinking: connect with the right networks, platforms, and financial institutions so Stripe becomes the default infrastructure layer for digital commerce. In 2026, this ecosystem approach is what makes Stripe faster to adopt, harder to replace, and easier to expand across industries.

1) Stripe’s Collaboration Philosophy

Stripe partners with companies that already own distribution, trust, or infrastructure. Instead of competing with every player, Stripe often becomes the “engine under the hood,” powering payments, billing, and financial workflows while partners focus on customer experience.

This creates a win-win loop:

- Partners gain a reliable financial stack

- Stripe gains reach, volume, and long-term integrations

2) Key Partnership Types That Strengthen Stripe

Technology & API Partners

- Ecommerce platforms, CRM tools, SaaS ecosystems

- Checkout and conversion optimization tools

- Analytics, reporting, and automation integrations

Payment & Banking Alliances

- Card networks and acquiring banks

- Local payment method providers (region-specific rails)

- Currency conversion and settlement partners

Marketplace & Platform Alliances

- Multi-vendor ecommerce platforms

- On-demand service marketplaces

- Subscription-first SaaS platforms needing billing + invoicing

Marketing & Distribution Partners

- Startup accelerators and developer communities

- Agency networks building Stripe-powered solutions

- Platform marketplaces that recommend Stripe by default

Regulatory & Expansion Alliances

- Compliance providers for KYC/AML workflows

- Identity verification and fraud intelligence partners

- Regional partners enabling faster country expansion

3) Ecosystem Strategy: Why It Creates a Competitive Moat

Stripe’s ecosystem becomes a moat because it builds network effects through integration density:

- The more platforms that integrate Stripe, the more merchants adopt it

- The more merchants adopt it, the more partners build around it

- The ecosystem compounds, making Stripe “standard infrastructure”

Stripe also monetizes within this ecosystem by:

- charging for premium workflows (Connect, Billing, Radar)

- increasing revenue per customer through add-ons

- reducing churn because partner integrations increase switching costs

For founders, the key lesson is clear: a platform scales faster when partnerships reduce friction, expand distribution, and strengthen trust. This is exactly how Miracuves helps entrepreneurs design scalable ecosystems—by building app architectures that are integration-ready from day one.

Read more : Best Stripe Clone Scripts 2025: Build a Scalable Global Payment Infrastructure for Your Startup

Growth Strategy & Scaling Mechanisms

Stripe’s growth story is a masterclass in scaling a platform business without depending on hype. Instead of chasing consumer attention, Stripe scaled by becoming critical infrastructure for the internet economy. In 2026, Stripe continues to grow because it expands across more industries, more countries, and more financial workflows—while staying developer-first.

1) Stripe’s Growth Engines (What Drives Scale)

Organic Growth (Developer Virality)

Stripe’s strongest engine is product-led adoption:

- Developers recommend it because it’s easy to integrate

- Founders choose it because it reduces time-to-launch

- Teams stick with it because it’s reliable at scale

This creates a “quiet virality” inside product teams.

Referral Loops & Ecosystem Expansion

- Platforms integrate Stripe → merchants adopt Stripe

- Merchants grow → transaction volume grows

- Growth unlocks new Stripe products → revenue per customer increases

Paid Acquisition & Enterprise Sales

Stripe also scales through:

- enterprise partnerships and custom contracts

- account-based sales for high-volume merchants

- large platform deals that bring in thousands of sub-merchants

New Product Lines (Expansion Revenue)

Stripe grows not only by processing more payments, but by expanding into:

- subscriptions and billing automation

- marketplace payouts and onboarding

- fraud prevention and risk tools

- embedded finance capabilities

Geographic Expansion Model

Stripe expands market-by-market by:

- adding local payment methods

- enabling local compliance support

- optimizing conversion for regional checkout behavior

2) Scaling Challenges Stripe Faced (And How It Solved Them)

Challenge 1: Operational Complexity at Global Scale

As Stripe grows, it must handle:

- multiple currencies and settlement rules

- country-specific regulations

- varying fraud patterns and risk profiles

Solution

- strong compliance systems + modular infrastructure

- region-ready payment routing and risk engines

Challenge 2: Infrastructure Limits & Reliability Pressure

In fintech, even small downtime creates major business losses.

Solution

- heavy investment in uptime, redundancy, and monitoring

- enterprise-grade incident response practices

Challenge 3: Regulatory Barriers

Payments and embedded finance require strict compliance.

Solution

- partnerships with banks and regulators

- scalable onboarding (KYC/AML) workflows

Challenge 4: Competition & Pricing Pressure

Payment processing can become commoditized.

Solution

Stripe defends itself by:

- offering more value than “just payments”

- increasing switching costs through deeper integrations (Billing + Connect)

- improving conversion and authorization performance

3) What Founders Should Learn From Stripe’s Scaling Playbook

Stripe proves that platform growth becomes unstoppable when:

- your product becomes infrastructure, not a feature

- your expansion is modular (add-on products)

- your ecosystem creates distribution advantages

This is also why Miracuves helps founders build platform-ready apps with scalable architecture, monetization layers, and growth mechanics—so you can scale like Stripe, but in your niche market.

Growth Strategy & Scaling Mechanisms

Stripe’s growth story is a masterclass in scaling a platform without becoming dependent on hype. Instead of chasing consumer branding, Stripe scaled through developers, product adoption, and compounding infrastructure demand. In 2026, its growth is driven by the fact that every online business needs payments, and every growing business needs deeper financial tools.

1) Growth Engines (What Actually Drives Stripe’s Scale)

Organic Growth (Developer Virality)

Stripe grows because developers recommend it.

- Clean documentation and fast onboarding

- Strong “first success” moment (first payment processed)

- Easy integrations that reduce build time for startups

Referral Loops & Word-of-Mouth

- Founders recommend Stripe to other founders

- Agencies implement Stripe repeatedly across clients

- SaaS platforms embed Stripe as the default option

Paid Marketing & Enterprise Acquisition

Stripe uses paid growth selectively, mainly for:

- enterprise accounts with high payment volume

- vertical-specific solutions (SaaS, ecommerce, platforms)

- strategic markets where compliance is complex

New Product Lines (Expansion Revenue)

Stripe doesn’t just grow volume—it grows “wallet share” per customer by adding:

- Billing for subscriptions

- Connect for marketplaces

- Radar for fraud

- Issuing and embedded finance tools

Geographic Expansion Models

Stripe scales globally by:

- adding local payment methods per country

- enabling multi-currency settlement

- improving compliance workflows region-by-region

2) Scaling Challenges & How Stripe Solves Them

Stripe’s scaling challenges are the same ones most platforms face—just at a much bigger level.

Challenge: Operational Complexity

- Different countries have different rules, payment methods, and settlement timelines

Solution: modular infrastructure + region-specific compliance layers

Challenge: Fraud, Chargebacks & Risk

- More volume attracts more fraud attempts

Solution: machine-learning risk tools + adaptive fraud rules (Radar)

Challenge: Uptime and Reliability at Scale

- Even small downtime impacts thousands of businesses

Solution: heavy investment in infrastructure, redundancy, monitoring

Challenge: Regulation and Trust

- Fintech platforms must stay compliant while moving fast

Solution: partnerships + built-in compliance workflows + constant audits

3) The Stripe Scaling Formula (Founder-Friendly Summary)

Stripe grows through a simple loop:

Reduce integration friction → increase adoption → expand product depth → increase retention → scale globally

This is also the blueprint Miracuves follows when building scalable platforms: we focus on core product-market fit first, then design growth-ready systems like onboarding, payments, retention hooks, and monetization layers that can scale without rebuilding.

Competitive Strategy & Market Defense

Stripe operates in one of the most competitive industries in the world—payments and fintech infrastructure. In 2026, the market is crowded with payment gateways, banks, and all-in-one commerce platforms. Stripe stays ahead because it doesn’t compete only on price. It competes on trust, developer experience, product depth, and ecosystem lock-in.

1) Stripe’s Competitive Advantages (Why It Wins)

Network Effects + Switching Barriers

Once a business integrates Stripe deeply into:

- checkout

- subscriptions

- payouts

- fraud workflows

Switching becomes risky and expensive. This creates a strong retention moat.

Brand Equity + Trust

Stripe is trusted because it consistently delivers:

- uptime and stability

- secure payment handling

- compliance-ready infrastructure

In fintech, trust is not marketing—it’s survival.

Developer-First Advantage

Stripe’s documentation and APIs are a competitive weapon.

- Faster integrations = faster launches

- Better dev experience = more adoption

- Better tooling = stronger ecosystem building

Innovation in Infrastructure

Stripe stays competitive by improving:

- payment success rates (authorization optimization)

- global payment method coverage

- fraud detection and risk controls

- modular product expansion (Billing, Connect, Radar, Issuing)

Data-Driven Personalization

Stripe uses transaction-level insights to improve:

- fraud filtering accuracy

- checkout conversion performance

- dispute reduction workflows

This creates continuous performance improvement at scale.

2) Market Defense Tactics (How Stripe Protects Its Position)

Handling New Entrants & Pricing Wars

Instead of racing to the lowest price, Stripe defends by:

- offering higher conversion + reliability value

- bundling products that reduce total cost of ownership

- positioning as “infrastructure,” not a commodity gateway

Strategic Feature Rollouts

Stripe releases features at the right time to stay ahead, such as:

- faster onboarding flows

- better subscription recovery tools

- marketplace-grade payouts and compliance support

This prevents competitors from winning on convenience.

Partnership Moves to Protect Distribution

Stripe defends market share by embedding itself into:

- ecommerce platforms

- SaaS ecosystems

- marketplace builders

When Stripe becomes the default integration, competitors struggle to break in.

Expansion Into Adjacent Categories

Stripe protects itself by expanding beyond payments into:

- billing and invoicing

- embedded finance tools

- risk and compliance systems

So even if payment processing becomes commoditized, Stripe still wins through depth.

3) Key Founder Insight

Stripe’s defense strategy proves one big lesson:

In competitive markets, the winner is not the cheapest—it’s the platform that becomes the most embedded.

That’s why Miracuves helps entrepreneurs build platform ecosystems with:

- scalable architecture

- modular monetization

- integration-ready design

- long-term retention mechanics

Because in 2026, the best business models are the ones that are hard to replace.

Lessons for Entrepreneurs & Implementation

Stripe’s journey offers one of the clearest lessons in modern platform building: you don’t need a consumer app with millions of followers to become a billion-dollar company. You can win by becoming the invisible infrastructure that other businesses depend on. The Business Model of Stripe proves that long-term scale comes from solving painful operational problems—payments, trust, compliance, and global expansion—better than anyone else.

1) Key Factors Behind Stripe’s Success

Here’s what Stripe did right (and what founders can copy):

- Developer-first product design → faster adoption and stronger word-of-mouth

- Simple onboarding + fast activation → users reach “first value” quickly

- Trust as a core product feature → uptime, security, compliance

- Layered monetization → payments first, then upsell Billing, Connect, Radar

- Global-ready infrastructure → local payment methods + multi-currency scaling

- Ecosystem thinking → partners and platforms become distribution engines

2) Replicable Principles for Startups

Even if you’re not building fintech, Stripe’s model applies to marketplaces, SaaS, and on-demand platforms:

- Build a core engine first (one clear problem, one killer workflow)

- Create a platform layer (APIs, automation, integrations, dashboards)

- Monetize based on usage and value, not only fixed pricing

- Make your product hard to replace through deep workflow integration

- Design for retention, not only acquisition

3) Common Mistakes to Avoid

Many founders fail because they do the opposite of Stripe:

- Building too many features before product-market fit

- Ignoring reliability, support, and trust signals

- Underestimating compliance and risk in multi-user platforms

- Relying on discounts instead of value-driven pricing

- Scaling marketing before the product experience is stable

4) Adaptation Strategy for Local or Niche Markets

You can adapt Stripe-like thinking even in a regional business:

- Focus on one niche (education payments, logistics payouts, service marketplaces)

- Start with the most common payment flow, then expand

- Add “trust layers” early: verification, dispute handling, fraud protection

- Build modular upgrades: subscriptions, commissions, premium tools

5) Implementation Timeline + Investment Priorities

A practical Stripe-inspired build plan for founders:

- Phase 1 : MVP + core payment workflow + onboarding

- Phase 2 : dashboard + automation + analytics + retention hooks

- Phase 3 : add monetization layers (subscriptions, commissions, add-ons)

- Phase 4 : scale infrastructure + partnerships + expansion markets

Ready to implement Stripe’s proven business model for your market? Miracuves builds scalable platforms with tested business models and growth mechanisms. We’ve helped entrepreneurs launch profitable apps. Get your free business model consultation today.

Conclusion

Stripe’s success proves a powerful truth about platform economies in 2026: the biggest winners are often the companies customers don’t “see,” but can’t operate without. The Business Model of Stripe shows how solving one core pain—online payments—can evolve into a complete financial infrastructure layer for global digital businesses. Stripe didn’t scale by chasing trends. It scaled by earning trust, reducing complexity, and expanding its product depth step-by-step. For entrepreneurs, the bigger lesson is clear: sustainable growth comes from building systems that are reliable, repeatable, and scalable across markets. In the future, the strongest platforms won’t just offer features—they’ll offer foundations that power entire industries.

FAQs

What type of business model does Stripe use?

Stripe uses a hybrid B2B platform model that combines payment infrastructure with usage-based SaaS tools like billing, fraud prevention, and marketplace payouts.

How does Stripe’s model create value?

Stripe creates value by simplifying complex financial workflows—payments, subscriptions, compliance, and payouts—so businesses can scale faster with less technical and operational burden.

What are Stripe’s key success factors?

Its biggest success factors are developer-first design, high reliability, strong security, global scalability, and layered monetization through multiple products.

How scalable is Stripe’s business model?

Highly scalable. Stripe grows automatically with customer transaction volume and expands revenue through add-ons like Billing, Connect, and Radar.

What are the biggest challenges in Stripe’s model?

Major challenges include regulatory compliance, fraud risk, infrastructure uptime demands, and competition from banks and payment providers.

How can entrepreneurs adapt it to their region?

Start with one strong payment workflow for a niche market, then add trust layers like verification and dispute handling, followed by monetization add-ons.

What are alternatives to this model?

Alternatives to Stripe’s model include a subscription-only SaaS model, marketplace commission model, and enterprise licensing model for predictable recurring revenue.

You can also use a payment aggregator + service bundle model, where payments are the entry point and profits come from bundled tools like billing, fraud, and payouts.

How has Stripe evolved over time?

Stripe evolved from simple card processing into a full financial infrastructure ecosystem including billing, fraud tools, marketplace payouts, and embedded finance products.

Related Article :