Key Takeaways

- A Wise clone script helps fintech startups launch an international money transfer platform faster than building from scratch.

- Senders, recipients, compliance teams, payment partners, and admins need secure and connected transfer workflows.

- Multi-currency accounts, real-time exchange rates, KYC, transfers, fee management, and tracking are core features.

- Pricing depends on transaction complexity, integrations, compliance requirements, architecture, and customization.

- A strong Wise-style app can reduce launch time while supporting transparent and scalable cross-border payments.

Feature Signals

- Users need simple onboarding, identity verification, recipient management, live rates, fee visibility, and transfer tracking.

- Payment workflows need multi-currency wallets, bank transfers, card payments, payout options, and transaction records.

- Admins need control over users, exchange-rate margins, transfer limits, fees, verifications, disputes, and reports.

- Compliance teams need KYC, transaction monitoring, risk alerts, audit logs, geo-restrictions, and account-review tools.

- Real-time notifications keep users updated on verification, payment receipt, transfer progress, completion, and failed transactions.

Real Insights

- A money transfer platform needs transparent rates, reliable transaction logic, and regulatory planning before it can scale.

- Weak exchange-rate or fee calculations can create financial disputes and reduce customer confidence.

- Revenue can come from FX margins, transfer fees, premium plans, faster payouts, and partner API access.

- Founders should include the cost of rate feeds, identity verification, banking integrations, refunds, and chargeback handling.

- Miracuves builds Wise Clone apps with cross-border transfers, multi-currency wallets, KYC workflows, fee controls, secure payments, and admin management.

Choosing a Wise clone script is not simply a matter of finding the longest feature list or the lowest quoted price. For a fintech founder, remittance operator, agency, or payment business, the more important question is whether the platform can support real cross-border transactions, multi-currency operations, verification workflows, administrative control, and future expansion.

A ready-made product can reduce the time required to enter the market, but only when its architecture and operational controls match the intended business model. Founders who want to examine an existing product can review Miracuves’ white-label cross-border payment platform and explore its mobile, web, and admin workflows.

This guide explains how to compare Wise clone scripts based on business value, features, pricing factors, monetization, security, customization, administration, and launch readiness. It is designed to help you shortlist the right product foundation without treating every money transfer script as interchangeable

What Is a Wise Clone Script?

A Wise clone script is a ready-made software foundation for building a branded international money transfer or multi-currency payment platform.

Instead of developing every wallet, recipient, exchange-rate, transfer, verification, reporting, and administrative workflow from zero, the business starts with an existing product architecture. That foundation can then be rebranded, configured, integrated, and customized around the target market.

A Wise-style platform may support use cases such as:

- Consumer remittances

- Freelancer and contractor payments

- International supplier payments

- Multi-currency accounts

- Business payouts

- Global payroll workflows

- Payment requests and invoicing

- Regional money transfer corridors

- Embedded payment services

The purpose is not to copy Wise’s branding, interface, trademarks, or proprietary systems. The purpose is to use a proven cross-border payment model as a starting point for an original product with its own brand, market, pricing, financial partners, and operating structure.

Read More: What is a Wise App and How Does It Work?

Why Founders Consider a Wise-Style App

Cross-border payments remain difficult for many individuals and businesses. Users may face unclear fees, exchange-rate markups, limited payout options, slow processing, complicated verification, and poor transaction visibility.

A focused international money transfer app can address a specific part of this problem.

The strongest opportunities often come from serving a clearly defined audience rather than trying to become a universal financial platform immediately.

Diaspora and Remittance Communities

A platform can focus on users sending money between selected countries. This gives the operator a narrower set of transfer corridors, payout methods, customer-support requirements, and marketing messages to manage during the first launch stage.

Freelancers and Remote Professionals

Freelancers may need multi-currency balances, payment requests, client receipts, currency conversion, and withdrawals to local accounts.

A Wise-style app built for this group can prioritize payment collection, transaction records, invoicing, and simple conversion workflows.

Small and Medium-Sized Businesses

Businesses may need supplier payments, team permissions, batch transfers, approval workflows, expense records, and financial reporting.

This creates opportunities for subscriptions and higher-value business accounts beyond individual transfer fees.

Global Payroll and Contractor Payments

Companies with distributed teams need tools for paying employees, contractors, and service providers across markets.

A specialized cross-border payment platform can combine recipient management, approval workflows, bulk transfers, reports, and transaction tracking.

Industry-Specific Payments

Education providers, healthcare operators, travel businesses, marketplaces, property platforms, and agencies may need international payment workflows tailored to their operations.

For additional category research, explore Miracuves’ fintech app insights and solutions.

Business Value of Starting With a Ready-Made Product

The value of a ready-made script is not limited to development speed.

A structured product foundation can help founders reach important business decisions sooner:

- Which transfer corridor has the strongest demand?

- Which users complete identity verification?

- Which fee structure is acceptable?

- Which payment and payout methods matter most?

- Which user segment completes repeat transfers?

- Where do transaction failures occur?

- How much operational support is required?

- Which integrations should be prioritized?

- What administrative controls are missing?

These questions are difficult to answer through planning documents alone. They require a working product, realistic workflows, and actual user feedback.

A ready-made foundation can help move the business toward this validation stage without rebuilding standard wallet, recipient, transfer, reporting, and admin modules from the beginning.

However, faster deployment does not remove the need for due diligence. Founders still need to inspect the code ownership terms, integration scope, security approach, customization boundaries, support package, and operational readiness.

Read More: Revolut vs Wise Business Model: What Fintech Founders Should Learn Before Building

Must-Have Features in a Wise Clone Script

A long feature list does not automatically make a product launch-ready. Each major feature should solve a real user, business, or operational problem.

1. Multi-Currency Accounts and Wallet Records

Users should be able to view supported currency balances, account activity, conversion history, incoming payments, outgoing transfers, refunds, and adjustments.

The platform must maintain clear wallet and transaction records behind the interface. This matters because balance errors, duplicate updates, failed settlements, and unclear transaction states can quickly damage trust.

Founders should ask:

- How are balances calculated?

- How are pending transactions represented?

- How are refunds and reversals handled?

- Can the platform support additional currencies?

- Are wallet and transaction records auditable?

- Can administrators make controlled adjustments?

2. Currency Conversion and Rate Management

The platform should support exchange-rate feeds, conversion calculations, configurable margins, corridor-specific pricing, and transparent customer-facing information.

Users should be able to see:

- The source currency

- The destination currency

- The applied exchange rate

- The transfer fee

- The amount the recipient is expected to receive

- The estimated processing status

Administrators should be able to manage rate providers, pricing rules, margins, and exceptions where appropriate.

Founders must also understand what happens when a rate provider becomes unavailable, a rate changes during a transaction, or a transfer remains pending.

3. Recipient Management

Users should be able to add, verify, edit, save, and select recipients without repeatedly entering the same information.

Recipient data may include:

- Full name

- Country

- Bank or payout details

- Account number or payment identifier

- Transfer purpose

- Relationship information where required

- Supporting information for specific corridors

The platform should validate recipient information and reduce preventable errors before the transfer reaches a payment or payout partner.

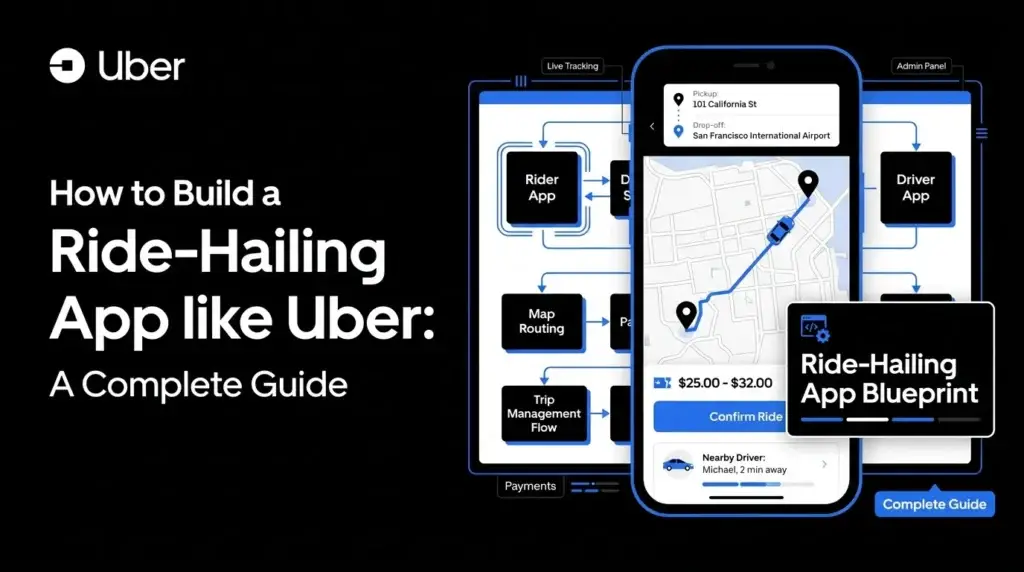

4. International Transfer Workflows

A complete transfer workflow should guide the user from currency selection to payment confirmation and transaction tracking.

The flow may include:

- Selecting the source and destination currencies

- Entering the transfer amount

- Reviewing the exchange rate and fees

- Selecting or adding a recipient

- Choosing a payment method

- Completing verification where required

- Confirming the transaction

- Monitoring the transfer status

- Receiving a receipt or notification

The backend should clearly distinguish between initiated, pending, processing, completed, failed, refunded, cancelled, and manually reviewed transfers.

5. User and Business Verification

A financial platform may need to support individual verification, business verification, document collection, risk checks, manual review, and approval workflows.

Important capabilities include:

- Identity-document submission

- Address verification

- Selfie or liveness workflow support

- Business-registration document collection

- Beneficial-owner information

- Verification status tracking

- Manual review queues

- Rejection and resubmission workflows

- Audit records

The platform can support KYC and KYB workflows, but final verification requirements depend on the business model, operating jurisdiction, financial partners, and legal advice.

6. Transaction Monitoring and Risk Controls

The administrative team should be able to identify activity that requires investigation.

Useful controls may include:

- Transaction limits

- Velocity checks

- Unusual login alerts

- Repeated failed transfers

- High-value transaction flags

- Country or corridor restrictions

- Suspicious recipient patterns

- Device and location changes

- Manual review queues

- Account restrictions

- Activity logs

These controls help the operating team investigate risk. They do not guarantee regulatory compliance or eliminate fraud.

7. Fee Management

The operator should be able to configure how the platform earns revenue.

Possible fee structures include:

- Fixed transfer fees

- Percentage-based fees

- Corridor-specific pricing

- Payment-method fees

- Priority-transfer fees

- Business-account subscriptions

- Volume-based pricing

- Currency-conversion margins

The fee engine should present pricing clearly before the customer confirms a transaction.

8. Payment and Payout Integrations

A cross-border payment platform may need integrations with:

- Banking partners

- Payment gateways

- Card processors

- Payout networks

- Open-banking providers

- Local payment rails

- Mobile money services

- Identity-verification providers

- Exchange-rate data providers

- Notification services

- Accounting or reporting tools

Founders should confirm which integrations are included, which are already supported, and which require separate development or commercial agreements.

9. Notifications and Transaction Updates

Users should receive clear updates when:

- Verification is required

- A transfer has been initiated

- A payment has been received

- A transaction is under review

- A transfer has been completed

- A transfer has failed

- A refund has been processed

- Account information changes

- Suspicious activity is detected

Notifications may be delivered through email, SMS, push notifications, or in-app messages.

10. Reports and Statements

Users may need account statements, transaction receipts, fee records, currency-conversion history, and downloadable reports.

Administrators may need:

- Transaction summaries

- Revenue reports

- Fee reports

- Verification reports

- Failed-transfer reports

- Corridor performance

- User activity

- Risk and review reports

- Reconciliation exports

- Audit logs

Reporting should support financial operations and customer support, not only display vanity metrics.

Read More: How Wise Clone Platforms Connect With ERP, CRM, and Accounting Tools

Feature-to-Business-Value Comparison

| Feature | User Value | Business Value | Founder Evaluation Question |

|---|---|---|---|

| Multi-currency wallet | Hold and manage supported currencies | Encourages repeat usage | Can balances, conversions, refunds, and adjustments be tracked accurately? |

| FX engine | Clear exchange-rate calculation | Supports conversion revenue | Can margins and corridor pricing be configured? |

| Recipient management | Faster repeat transfers | Improves retention | Can recipient fields adapt to different markets? |

| KYC and KYB workflows | Structured onboarding | Supports risk operations | Can cases be reviewed and audited? |

| Transaction monitoring | Safer platform activity | Improves operational control | Which alerts and limits can administrators configure? |

| Admin dashboard | Faster issue resolution | Reduces operational dependency | Can routine settings be changed without developers? |

| API integrations | More payment options | Supports market expansion | Which providers are included or already supported? |

| Reports and audit logs | Greater transparency | Supports reconciliation and reviews | Can records be exported and traced? |

How to Compare Wise Clone Script Providers

A provider comparison should use documented criteria rather than generic “best platform” rankings.

Request a Working Demonstration

Review the actual user application, web platform, and admin dashboard.

A presentation or feature document cannot show how the product handles:

- Failed transfers

- Verification reviews

- Fee calculation

- Transaction states

- Account restrictions

- Refunds

- Reports

- Administrative permissions

- Integration errors

- User-support cases

Ask to test the journeys most relevant to your launch model.

Examine the Admin Dashboard

The admin dashboard is where the platform operator manages routine business activity.

Ask the provider to demonstrate how administrators:

- Review user accounts

- Approve or reject verification cases

- Monitor transactions

- Configure fees and limits

- Manage currencies and corridors

- Investigate flagged activity

- Process refunds

- Export reports

- Create roles and permissions

- Update platform settings

A polished user interface cannot compensate for weak operational control.

Clarify What the Price Includes

The proposal should state whether the price includes:

- Android application

- iOS application

- Web application

- Admin dashboard

- Source code

- White-label branding

- Interface customization

- Deployment assistance

- App-store publishing

- Server configuration

- Third-party integrations

- Technical documentation

- Bug-fix support

- Product updates

- Ongoing maintenance

Do not assume that a phrase such as “complete platform” includes every item.

Confirm Source-Code and Licensing Terms

Ask whether you receive the complete source code and what rights are granted.

Review:

- Code ownership

- Modification rights

- Deployment restrictions

- Domain restrictions

- Resale restrictions

- Update rights

- Third-party libraries

- Recurring licence fees

- Access to repositories

- Documentation availability

The contract should explain these terms clearly.

Assess Integration Readiness

Ask which banking, payout, verification, payment, exchange-rate, notification, and analytics providers the platform can support.

Integration readiness should include more than a list of logos. Confirm:

- Whether the integration is already functioning

- Whether credentials are supplied by you

- Whether the provider supports your country

- Whether separate onboarding is required

- Whether additional development is charged

- How webhooks and failures are handled

- How integration activity is logged

Review the Technology Foundation

The technology stack should match the scale, integrations, maintenance model, and development resources of the project.

The important questions are not limited to the names of frameworks.

Ask:

- Is the code documented?

- Can the architecture support additional modules?

- How are financial records structured?

- How are APIs secured?

- How are background processes managed?

- How are failures retried?

- How are audit records stored?

- How are updates deployed?

- Can the platform be monitored?

- Can another development team maintain the product?

Understand the Support Model

Confirm the difference between:

- Bug fixing

- Configuration assistance

- Integration support

- Product updates

- Feature customization

- Infrastructure management

- Security maintenance

- Emergency support

A support package may cover defects but not new integrations or feature requests.

What Determines Wise Clone Script Pricing?

The cost of an international money transfer platform depends less on the number of screens and more on the workflows behind them.

Platform Coverage

A mobile-only product has a different scope from a platform that includes Android, iOS, web, business accounts, an admin dashboard, and partner APIs.

Wallet and Transaction Complexity

Multi-currency balances, transfers, refunds, conversions, adjustments, transaction histories, and settlement records require structured backend logic.

Financial Integrations

Banking, payment, payout, identity, card, and rate-provider integrations can add implementation and testing requirements.

Each provider may also have its own commercial onboarding process and usage charges.

Verification and Risk Workflows

Individual verification, business verification, sanctions screening, transaction monitoring, manual review queues, account restrictions, and audit records can affect implementation scope.

Admin and Reporting Requirements

Basic account management is different from a complete operational dashboard with configurable fees, risk queues, reconciliation reports, role-based permissions, and audit visibility.

Customization

Brand colors and logos are relatively straightforward.

Deeper changes may include:

- New account types

- Different transfer journeys

- Country-specific recipient fields

- Business approval workflows

- Custom reports

- Additional currencies

- New financial integrations

- Subscription plans

- API access

- Team roles

- Corridor-specific controls

Infrastructure and Deployment

The total budget may need to include hosting, monitoring, backups, logging, security configuration, domain setup, certificates, app-store submission, and deployment assistance.

Support and Maintenance

Ongoing costs may include bug fixes, infrastructure monitoring, framework updates, security patches, integration maintenance, and product enhancements.

For a more detailed breakdown, review the cost factors behind building a Wise-style money transfer platform.

Read More: Pre-launch vs Post-launch Marketing for Wise Clone Startups

Miracuves Wise-Like Platform Solution Cost and Tech Stack

Miracuves Pricing for a Wise-Like Money Transfer and Remittance Platform for $12,999 USD (One-Time Price) in just 6 days

Get a fully developed, deployment-ready cross-border money transfer platform modeled after Wise. Built on a modern JavaScript foundation, this complete package includes everything you need to launch and scale a digital remittance and international payment business:

Core Workflows: User registration, KYC verification, sender and receiver management, currency selection, exchange rate display, transfer initiation, payment processing, transaction tracking, recipient notifications, and transfer history.

Built-in Revenue Logic: Transfer fees, foreign exchange margins, premium transfer options, business account fees, international payout charges, wallet-based monetization, partner banking fees, and transaction-based revenue.

Management Hub: Centralized admin dashboard, user management, KYC review, transaction monitoring, currency controls, exchange rate management, payment records, payout tracking, refund handling, compliance logs, and remittance analytics.

Launch-Ready: Fully prepared for your custom branding, configuration, payment gateway setup, currency setup, transfer workflow configuration, compliance workflow setup, and immediate market entry.

Why Is Wise-Like Platform Development More Affordable?

Most cross-border payment platforms become expensive when businesses choose fully custom development from scratch. A Wise-style platform usually needs user onboarding, KYC workflows, currency exchange logic, transfer processing, recipient management, payment integrations, admin controls, transaction monitoring, security layers, and compliance-ready operations. Building every component separately can significantly increase both development cost and launch time.

We took a smarter, more practical approach:

You Aren’t Paying for Ground-Up Development: Our remittance and money transfer platform engine is already developed, tested, and ready to deploy. You avoid the inflated cost and extended timeline associated with building every payment workflow from scratch.

The Power of JavaScript: We built this solution on a modern JavaScript architecture that supports fast frontend performance, scalable API-driven workflows, real-time transaction updates, flexible integrations, and smooth admin operations.

You get a launch-ready Wise-like money transfer platform with practical remittance, currency exchange, payment, compliance, and monetization features, along with source code access and faster deployment.

Note: This cost is for the solution, re-branding, deployment, and source code only. Banking licenses, regulatory approvals, payment provider charges, third-party KYC services, liquidity partners, FX providers, hosting infrastructure, and custom security integrations are not included.

Read More: Wise App Features List: What Founders Can Learn from a Global Money Transfer App

Why the Admin Panel Matters as Much as the User App

The user-facing interface helps customers initiate transfers, but the admin dashboard determines whether the business can operate the platform effectively.

A practical admin panel should give authorized teams control over the following areas.

User and Account Management

Administrators should be able to:

- Review user profiles

- Check account status

- View verification progress

- Restrict or reactivate accounts

- Review login or device activity

- Examine transaction history

- Respond to support cases

Verification Review

The admin team may need to:

- Review submitted documents

- Request additional information

- Approve or reject cases

- Escalate high-risk users

- Track verification changes

- Record decisions

- Preserve review history

Transaction Oversight

Operations teams should be able to view:

- Pending transfers

- Completed transfers

- Failed transactions

- Refunds

- Transactions under review

- Payment and payout status

- Provider responses

- Fee calculations

- Currency-conversion details

Fee and Currency Configuration

The platform operator may need controlled access to:

- Supported currencies

- Transfer corridors

- Minimum and maximum amounts

- Exchange-rate margins

- Fixed fees

- Percentage fees

- User-tier pricing

- Payment-method charges

- Country restrictions

Risk and Fraud Monitoring

Authorized personnel should be able to view alerts, transaction patterns, account restrictions, review notes, suspicious activity flags, and supporting evidence.

Roles and Permissions

Support staff should not automatically receive the same permissions as finance, compliance, or senior administrators.

Role-based access helps reduce unnecessary exposure and creates clearer accountability.

Reporting and Audit Logs

The admin dashboard should preserve records of important activities, including:

- Verification decisions

- Fee changes

- Account restrictions

- Refunds

- Transfer interventions

- Permission changes

- Configuration changes

- Administrative logins

These records support troubleshooting, internal reviews, and operational accountability.

What Can Be Customized in a Wise-Style App?

Customization should begin with the business model, not just visual branding.

Brand and Interface Customization

Common changes include:

- Brand name

- Logo

- Color system

- Typography

- Icons

- Onboarding content

- Email templates

- Push-notification language

- Help and support content

Market and Corridor Configuration

A platform may need changes to:

- Supported countries

- Supported currencies

- Transfer limits

- Recipient fields

- Payment methods

- Payout methods

- Transfer-purpose options

- Fee rules

- Exchange-rate margins

- Verification requirements

User-Type Customization

Different platforms may serve:

- Individual users

- Freelancers

- Small businesses

- Finance teams

- Agencies

- Payroll operators

- Marketplace sellers

- API partners

Each audience may need different dashboards, permissions, reports, and financial workflows.

Operational Customization

The business may require:

- Manual approval steps

- Risk-review queues

- Custom reports

- Reconciliation exports

- Team permissions

- Support workflows

- Refund controls

- Dispute processes

- Provider-specific transaction states

Integration Customization

The platform may need to connect with region-specific financial providers, identity-verification tools, payout partners, analytics systems, or accounting software.

Before approving a project, document which changes are included as configuration and which require additional development.

Read More: How Wise Makes Money and What Startups Can Learn

Security Requirements for a Cross-Border Payment Platform

Security should be treated as a product foundation, not a feature added shortly before launch.

A money transfer platform may process identity records, account information, recipient details, transaction data, authentication credentials, and financial-provider responses.

The security plan should cover the mobile application, web platform, APIs, backend services, databases, admin dashboard, infrastructure, logs, and third-party integrations.

Encrypted Data Transfer

Data exchanged between users, applications, servers, and external providers should be protected during transmission.

Protected Data Storage

Sensitive data should be classified and protected based on its purpose, risk, and retention requirements.

The platform should avoid storing unnecessary information and should restrict access to sensitive records.

Authentication and Session Security

Security controls may include:

- Strong password requirements

- Multi-factor authentication

- Secure password recovery

- Session expiration

- Device or login monitoring

- Suspicious-login alerts

- Administrative access restrictions

Role-Based Access Control

Permissions should be assigned according to job responsibilities. Support, finance, compliance, operations, and technical teams should not receive unrestricted access by default.

Secure API Integrations

Financial and verification integrations should use secure credential storage, webhook validation, request authentication, error handling, monitoring, and controlled access.

Audit Logs

Important user, system, and administrative activities should be recorded in a way that supports investigation and accountability.

Monitoring and Incident Response

The operating team should define how it will:

- Detect unusual activity

- Respond to integration failures

- Restrict compromised accounts

- Investigate administrative activity

- Notify relevant teams

- Restore affected services

- Document incidents

For deeper technical reading, see these financial app encryption best practices.

Compliance and Legal Responsibilities

A software platform can support compliance workflows, but it cannot automatically make a business compliant or provide regulatory authorization.

Final requirements depend on:

- Operating country

- Customer location

- Transfer corridors

- Payment and payout partners

- Business structure

- Transaction model

- Funds-flow structure

- Data-handling practices

- Financial products offered

- Licensing framework

A cross-border payment platform may need to support:

- Customer identity verification

- Business verification

- AML review workflows

- Transaction monitoring

- Sanctions-screening integrations

- Risk scoring

- Suspicious-activity review

- Transfer limits

- Record keeping

- Audit logs

- Compliance reports

- Account restrictions

Legal and regulatory professionals should review the operating model before launch.

Do not assume that software access includes a banking licence, money-transfer licence, electronic-money authorization, card programme, or payment-provider relationship.

How a Wise-Style App Can Make Money

A cross-border payment platform can combine several revenue models. The right structure depends on the target users, financial partners, competition, and operating costs.

For broader strategic context, read the business model of Wise for startup founders.

Foreign Exchange Margin

The business may apply a margin to the exchange rate offered to the user.

The margin needs to remain commercially competitive while covering provider costs, operational expenses, risk, and customer acquisition.

Transfer Fees

Fees may be:

- Fixed

- Percentage-based

- Corridor-specific

- Payment-method-based

- Delivery-speed-based

- User-tier-based

- Volume-based

Pricing should be shown clearly before a transfer is confirmed.

Business Subscriptions

Business users may pay recurring fees for:

- Team accounts

- Approval workflows

- Batch transfers

- Invoicing

- Payroll support

- Advanced reporting

- Dedicated support

- Account-management tools

API Access

Other businesses may pay to use transfer, payout, currency, wallet, or account capabilities through an API.

This model requires reliable infrastructure, documentation, authentication, monitoring, limits, and partner support.

Premium Services

Potential premium services include:

- Priority support

- Faster review

- Higher limits

- Advanced reporting

- Specialized payment workflows

- Dedicated account management

- Additional business controls

Card and Payment Revenue

Where supported by licensed financial partners and the operating model, the platform may generate revenue through card, payment, or account-related services.

The availability and structure of this revenue depend on the relevant partners and jurisdictions.

Unit Economics Matter More Than Transaction Volume

High transfer volume does not automatically create a profitable platform.

The business must account for:

- Banking and payout charges

- Payment-processing fees

- Currency-conversion costs

- Verification charges

- Fraud losses

- Refunds and chargebacks

- Customer support

- Infrastructure

- Compliance operations

- Reconciliation

- Partner minimums

- Marketing and acquisition

- Product maintenance

Founders should calculate contribution margin by corridor, user segment, payment method, and transfer size.

A corridor that attracts many users may still be unattractive if payout costs, failure rates, fraud exposure, or support requirements are too high.

Hidden Costs Founders Should Plan For

The quoted software price may not include every expense required to operate the business.

Potential additional costs include:

- Foreign exchange data

- Identity-verification providers

- Business-verification providers

- Sanctions-screening tools

- Fraud-monitoring services

- Banking partner onboarding

- Payout network fees

- Payment gateway charges

- Card programme costs

- Cloud infrastructure

- Monitoring and backups

- Security reviews

- Legal and regulatory advice

- Compliance personnel

- Customer support

- Reconciliation tools

- App-store accounts

- Email, SMS, and push notifications

- Product maintenance

- New integrations

Request an inclusion-and-exclusion document before signing a development agreement.

It is also useful to review the common mistakes founders make while building a Wise-style platform.

A Practical Launch Process

A strong launch process starts with the market and operating model before moving into branding and deployment.

Step 1: Choose the Initial Customer Segment

Define whether the first users are individuals, freelancers, small businesses, payroll teams, agencies, or another specific group.

Avoid trying to serve every possible fintech audience at launch.

Step 2: Define the First Transfer Corridors

Choose the initial source countries, destination countries, currencies, payment methods, and payout methods.

A focused corridor strategy simplifies integration, support, compliance planning, pricing, and marketing.

Step 3: Confirm the Financial Operating Model

Determine which banks, payment providers, payout networks, verification vendors, and licensed partners are required.

Clarify how funds will move from sender to recipient.

Step 4: Map the Product Workflows

Document:

- Registration

- Verification

- Recipient creation

- Rate display

- Fee calculation

- Payment collection

- Transfer processing

- Transaction tracking

- Refunds

- Support

- Administrative review

- Reporting

Step 5: Review the User and Admin Demonstrations

Test the workflows before approving customization.

Ask the provider to show both successful and unsuccessful scenarios.

Step 6: Finalize Customization

Confirm:

- Branding

- User roles

- Currencies

- Corridors

- Fees

- Limits

- Reports

- Notifications

- Integrations

- Administrative permissions

Step 7: Complete Integration and Security Testing

Test:

- API responses

- Webhooks

- Authentication

- Permission boundaries

- Failed transactions

- Duplicate requests

- Refunds

- Rate changes

- Verification cases

- Reports

- Administrative actions

Step 8: Prepare Operations

Create processes for:

- Customer support

- Verification review

- Transaction investigation

- Provider failures

- Refunds

- Complaints

- Account restrictions

- Reconciliation

- Security incidents

Step 9: Launch With Controlled Scope

A focused first launch makes it easier to identify workflow problems and understand user behavior.

Expansion should follow operational stability and repeat usage rather than excitement alone.

Step 10: Measure and Improve

Monitor:

- Signup completion

- Verification completion

- First-transfer completion

- Transfer failure rate

- Repeat transfers

- Support requests

- Refund rate

- Revenue per transaction

- Corridor profitability

- User retention

Product deployment and customer acquisition should be planned together. Use this pre-launch and post-launch marketing guide to connect product readiness with demand generation.

Mistakes to Avoid When Selecting a Wise Clone Script

Choosing Based Only on Price

A lower quote may exclude source code, applications, integrations, deployment, customization, or post-launch support.

Compare scope before comparing totals.

Reviewing Only the User Interface

The admin dashboard, transaction logic, reporting, error handling, and integration architecture are more important than visual similarity.

Assuming Compliance Is Included

KYC and AML modules can support workflows, but software does not replace licensing, legal review, operating policies, or financial partnerships.

Ignoring the Funds Flow

The business must understand how money enters the system, where it is held, how it is converted, how it reaches the recipient, and which partner is responsible at each stage.

Launching Too Many Corridors

Every new corridor can introduce different recipient fields, partners, fees, risks, regulations, payout timelines, and customer-support issues.

Validate a focused market before expanding.

Failing to Document Customization

Verbal promises about features, integrations, and changes should be converted into written scope.

Ignoring Post-Launch Operations

A platform must be operated after it is deployed. Verification reviews, failed transfers, refunds, reporting, risk alerts, and customer support require clear ownership.

Ready-Made vs Custom Development

| Decision Area | Ready-Made Foundation | Custom Development |

| Launch speed | Faster when standard workflows fit | Longer because workflows are built from zero |

| Initial cost logic | Product foundation already exists | Budget covers full design and development |

| Flexibility | Strong within supported architecture | Greater potential flexibility |

| Product validation | Suitable for earlier market testing | Better when requirements are highly original |

| Technical risk | Depends on code quality and documentation | Depends on discovery, team quality, and execution |

| Integrations | Existing integrations may accelerate launch | Each integration may require new implementation |

| Best use case | Standard remittance or financial workflows | Specialized financial products or complex operations |

The correct choice depends on how unique the product needs to be.

A ready-made foundation is useful when the core business follows established wallet, recipient, transfer, reporting, and administrative patterns.

Custom development may be more appropriate when the project requires original ledger structures, institutional workflows, uncommon financial products, complex governance, or architecture that cannot be adapted from an existing platform.

Final Thoughts: Evaluate the Business Foundation, Not Just the Script

The purpose of a Wise clone script guide is not to declare one provider universally superior. It is to help founders determine whether a product can support their market, users, transfer corridors, integrations, revenue model, security expectations, and operational responsibilities.

A ready-made product can reduce the route to launch, but speed should not replace due diligence.

Before committing, founders should:

- Review the working app, web, and admin product

- Confirm the source-code and licensing terms

- Document the included modules

- Identify required integrations

- Understand the customization boundary

- Review security and administrative controls

- Confirm support and maintenance

- Plan legal and regulatory responsibilities

- Calculate ongoing operating costs

- Define a focused launch market

Once these requirements are clear, the next step is to compare them against an actual product and implementation proposal.

FAQs

What should founders check before buying a Wise clone script?

Review the working app, web platform, admin dashboard, integrations, security controls, ownership terms, and support scope. Confirm all features, customization requirements, deployment services, and exclusions in the final proposal.

How much does a Wise-style app cost?

The cost depends on features, platforms, supported currencies, integrations, compliance workflows, customization, and technical support. Miracuves currently lists its ready-made package at $12,999, subject to the final scope.

How long does it take to launch an international money transfer platform?

A ready-made platform can usually be launched faster than a fully custom product. Miracuves offers a standard six-day rollout, while advanced integrations or customization may require additional time.

Can a ready-made international money transfer app be customized?

Yes, it can be customized for branding, currencies, fee rules, workflows, reports, user roles, notifications, and integrations. The available customization depends on the product architecture and project requirements.

What should the admin panel of a cross-border payment platform manage?

The admin panel should manage users, verification cases, transfers, fees, limits, refunds, risk alerts, reports, and platform settings. It should also provide role-based access and activity logs.

Does a Wise clone script make a business legally compliant?

No, the software only supports KYC, AML, transaction-monitoring, reporting, and audit workflows. Final compliance depends on jurisdiction, licensing, financial partners, operating structure, and legal review.

How does a Wise-style app generate revenue?

Revenue can come from transfer fees, foreign exchange margins, subscriptions, API access, and premium services. The business should also account for banking, payout, verification, infrastructure, and compliance costs.

Is a Wise-style app suitable only for consumer remittances?

No, it can also support freelancer payments, business transfers, supplier payments, payroll, contractor payouts, and marketplace settlements. The workflows should be configured around the target audience.

Is it legal to build a Wise-style app?

Businesses can build an independently branded platform using common cross-border payment functionality. They must avoid copying protected branding or proprietary assets and obtain any licences required to operate.

Related Articles